9An Introduction to the Analysis of Dynamic Models

To build and analyse dynamic models, we need to understand the dynamics of state variables, which are a function of their own previous values: \(y_t=h(y_{t-1})\). The state variables govern the dynamics of the entire model (including the non-state variables). Typically, a model has multiple state variables that interact with each other over time. As shown in Chapter 2, we can simulate dynamic models numerically for a specific parameterisation. However, to study their dynamics in general, we need to mathematically analyse a system of difference (or differential) equations. This chapter provides a basic introduction to the mathematical tools to do this. It will help you understand the analytical discussions in the chapters on dynamic models but can be skipped if you are mostly interested in numerical simulation.

Solution of a single first-order linear difference equation

Consider a first-order linear difference equation:1

\[

y_t = a_0 + a_1y_{t-1}.

\]

One way to find a solution is through (manual) iteration:

The complementary function tells us about the ‘asymptotic stability’ of the equation: does \(y_t\) converge to \(y^*\) as \(t \rightarrow \infty\)?

For the case of a first-order difference equation, we can distinguish the following cases:

if \(|a_1|<1\), then the complementary function will converge to zero and \(y_t\) will approach the particular solution \(y^*\)

if \(|a_1|>1\), then the complementary function will grow exponentially or decay, and \(y_t\) will thus never converge to the particular solution \(y^*\)

if \(a_1=1\) and \(a_0 \neq0\), then \(y_t\) will grow linearly

if \(a_1=1\) and \(a_0 =0\), then \(y_t\) will not grow or fall forever, but it will also not approach a unique equilibrium (so-called Lyapunov stability)

To better understand the last two cases, note that if \(a_1=1\), a different (more general) approach to finding the particular solution is required: the so-called method of undetermined coefficients. This method consists of substituting a trial solution that contains undetermined coefficients into the difference equation and then attempting to solve for those coefficients. If the trial solution allows to pin down unique values for the coefficients, it constitutes a valid particular solution.

In the case above where \(a_1 \neq 1\), we could have used the trial solution \(y_t=y_{t-1}=y^*\) and then solve for \(y\) to obtain \(\frac{a_0}{1-a_1}\) as the particular solution. In the case where \(a_1=1\) and \(a_0 \neq 0\), we can use the trial solution \(y^*=kt\), which is a growing equilibrium. This yields \(y_t = k(t-1) + a_0\), which solves for \(k=a_0\), so that we can conclude \(y^*=a_0t\). This explains why we obtain linear growth. If \(a_1=1\) and \(a_0 =0\), we have \(y_t=y_{t-1}\), so that the equilibrium is given by the initial condition \(y_0\).

Solution of a linear system of difference equations

The solution approach just introduced can be extended to \(N\)-dimensional systems of linear difference equations of the form:

\[

y_t=a_0 + Ay_{t-1},

\]

where \(y_t\) is a \(1 \times N\) column vector and \(A\) an \(N \times N\) square matrix called the coefficient matrix.

If the inverse \((I-A)^{-1}\) exists, which requires \(det(I-A) \neq 0\), the solution will be of the form:

The problem with this generic solution is that it is difficult to assess what is going on: the dynamics of any variable in \(y_t\) will depend on a lengthy combination of the parameters in \(A\) that result from repeated matrix multiplication (\(A^t=A\times A\times A\times A...\)). This makes it impossible to assess whether the system converges to the particular solution. To address this problem, we can use a tool from linear algebra called matrix diagonalisation. Under certain conditions, a matrix \(A\) can be decomposed into the product of three matrices in which the matrix in the middle is diagonal. As we will see, this trick has a useful application to our problem.

A matrix \(A\) is diagonalisable if there is a diagonal matrix \(D\) and an invertible matrix \(P\) such that \(A=PDP^{-1}\). A major advantage of this decomposition is the following property: \(A^n = (PDP^{-1})^n = PD^nP^{-1}\).2 Thus, the \(nth\) power of the matrix \(A\), which typically yields very cumbersome expressions, simplifies to \(PD^nP^{-1}\), where the \(nth\) power of \(D\) is simply applied to each individual element on the main diagonal thanks to \(D\) being a diagonal matrix. As a result, diagonalisation allows us to write the complementary function in the solution to a system of difference equations as: \(PD^tP^{-1}y_0\). We can further define a vector of arbitrary constants \(c=P^{-1}y_0\) so that the complementary function becomes \(PD^tc\). The solution then takes the form \(y_t = y^* + PD^tP^{-1}[y_0- y^*] = y^* + PD^tc\)

For the first variable in the system, the solution would be:

where \(v_j\) are the column vectors of \(P\) and \(\lambda_i\) are the elements on the main diagonal of \(D\). The \(v_j\) are called the eigenvectors of the matrix \(A\) and the \(\lambda_i\) are its eigenvalues (more about them in a second). From this representation of the solution, the nature of the dynamics can easily be determined by looking at the eigenvalue \(\lambda\) that is largest in absolute terms. This is also called the ‘dominant eigenvalue’. Only if the dominant eigenvalue is \(|\lambda|<1\) will the system converge to \(y^*\). The elements \(v_{ij}\) of the eigenvectors act as multipliers on the eigenvalues and can thus switch off certain eigenvalues (if they happen to be zero) or amplify their dynamics both into the positive and negative domain (depending on their algebraic sign).

How can the diagonal matrix \(D\) be found? Notice that \(AP=PD\) can also be written as \(Av=\lambda v\). We can then write \(v(A-\lambda I)=0\). We want to find the solutions of this linear system other than \(v = 0\) (we don’t want the eigenvectors to be zero vectors, otherwise the solution to the dynamic system presented above wouldn’t work). This requires the determinant of the matrix \(A-\lambda I\) to become zero, i.e. \(det(A-\lambda I)=0\). Note that then there will be an infinite number of solutions for the eigenvectors.

Let’s consider an example. Let \(a_0=0\) for simplicity, so that the dynamic system is \(y_t = Ay_{t-1}\). Let the matrix \(A\) be given by: \[A=\begin{bmatrix}7 & -15 \\ 2 & -4 \end{bmatrix}.\]

This second-order polynomial solves for \(\lambda_1=2\) and \(\lambda_2=1\), which will be the elements on the diagonal of \(D\).

To find \(v_j\), substitute the \(\lambda_i\) into \(v_j(A-\lambda_iI)=0\). For \(\lambda_1=2\), we get \(5v_{11}- 15v_{21}=0\) and \(2v_{11}- 6v_{21}=0\), yielding the eigenvector \(v_1=\begin{bmatrix} 3 \\ 1\end{bmatrix}\). However, any scalar multiple of this eigenvector (other than zero) is admissible. It is thus common to normalise the eigenvectors by dividing through one of its elements. Dividing through by the first element yields the normalised eigenvector \(v_1=\begin{bmatrix} 1 \\ \frac{1}{3} \end{bmatrix}\).

For \(\lambda_2=1\), this yields \(6v_{12}- 15v_{22}=0\) and \(2v_{12}-5v_{22}=0\) from which we can deduce that \(v_2=\begin{bmatrix} 5 \\ 2\end{bmatrix}\). The normalised eigenvector is \(v_2=\begin{bmatrix} 1 \\ 0.4 \end{bmatrix}\).

Of course, you can also perform these calculations in R or Python:

#Clear the environment rm(list=ls(all=TRUE))## Find eigenvalues and eigenvectors of matrix# Define matrixJ=matrix(c(7, -15,2, -4), 2, 2, byrow=TRUE)# Obtain eigenvalues and eigenvectorsev=eigen(J)(evals=ev$values)

Before comparing these analytical results with those from a numerical simulation, let’s summarise the information we gain from the eigenvalues, eigenvectors, and arbitrary constants about the dynamics of the system:

since the dominant eigenvalue \(\lambda_1=2\) is larger than one, we know that the system is unstable

since both elements in the dominant eigenvector \(v_1=\begin{bmatrix} 1 \\ \frac{1}{3} \end{bmatrix}\) are non-zero, both variables in the system will be driven by that dominant eigenvalue

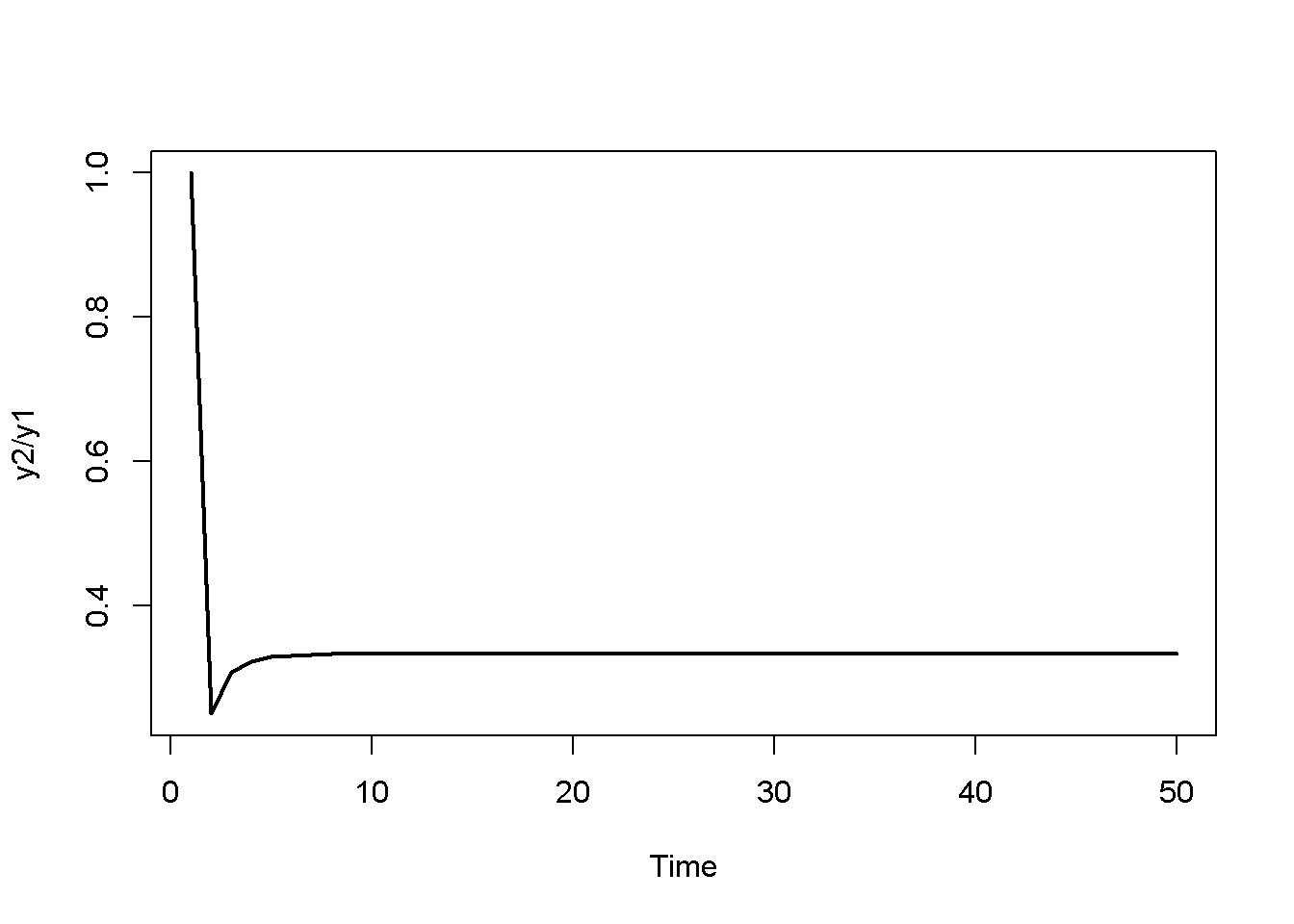

since both variables will grow or decay at the same rate, their ratio will be constant as \(t \rightarrow \infty\) and will approach a value that is given by the ratio of the elements in the dominant eigenvector

To see the last point, observe that in \(\frac{y_{2t}}{y_{1t}}=\frac{\frac{1}{3}c_{1}2^t + 0.4c_{2}1^t}{c_{1}2^t + c_{2}1^t}\) the first terms in the numerator and denominator, respectively, quickly dominate the second terms as \(t \rightarrow \infty\) (you can show this formally using L’Hopital’s rule). Thus, \(\frac{y_{2t}}{y_{1t}}\) will approach \(\frac{1}{3}\) as \(t \rightarrow \infty\). From an economic point of view, the systems thus displays a form of balanced growth, where both variables grow exponentially at the same rate.

Let us simulate the system and compare the results for, say, \(t=10\) with the analytical solution:

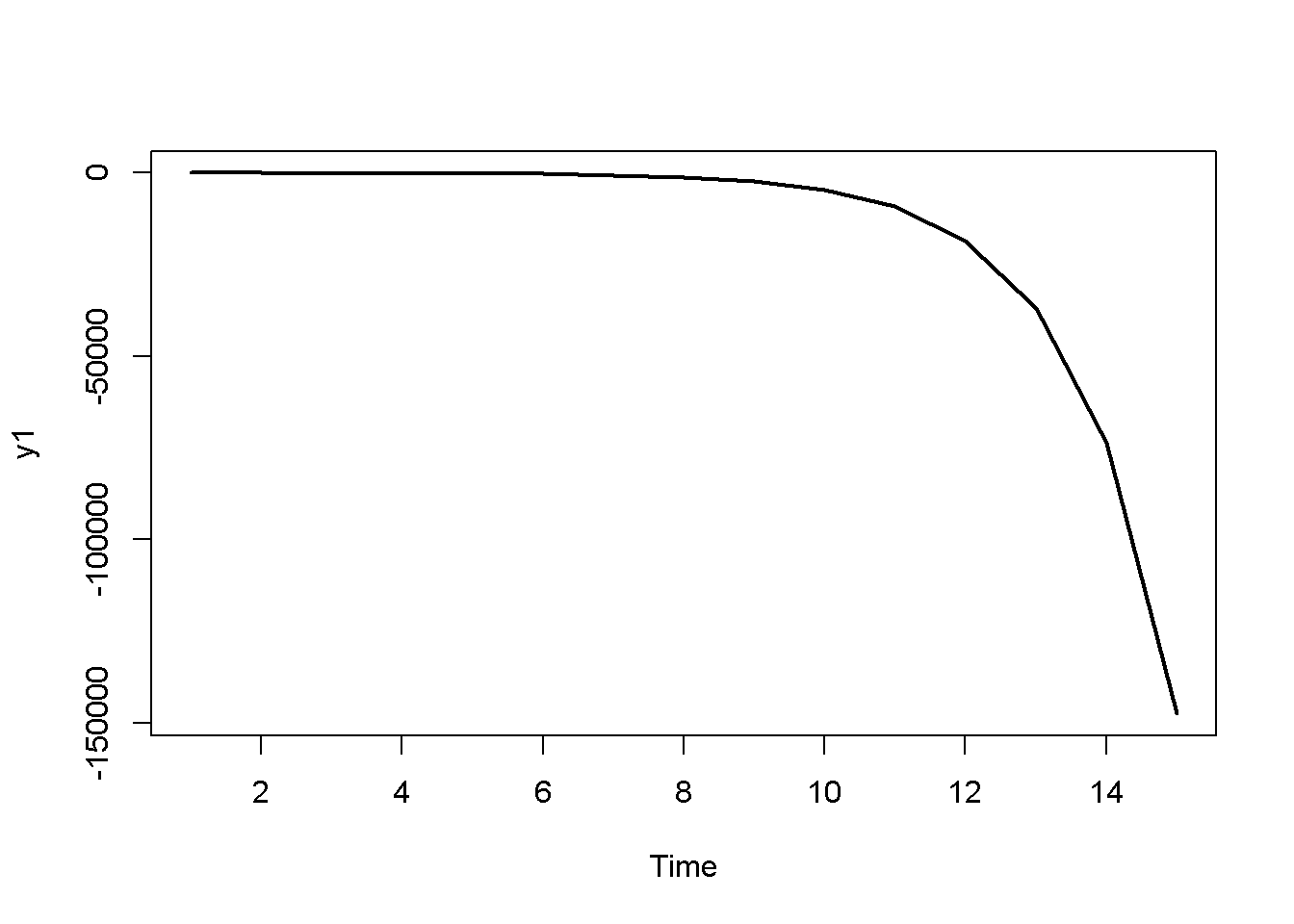

# Set number of periods for which you want to simulateQ=100# Construct matrices in which values for different periods will be stored; initialise at 1y1=matrix(data=1, nrow=1, ncol=Q)y2=matrix(data=1, nrow=1, ncol=Q)#Solve this system recursively based on the initialisationfor(tin2:Q){y1[,t]=J[1,1]*y1[, t-1]+J[1,2]*y2[, t-1]y2[,t]=J[2,1]*y1[, t-1]+J[2,2]*y2[, t-1]}# close time loop# Plot dynamics of y1plot(y1[1, 1:15],type="l", col=1, lwd=2, lty=1, xlab="Time", ylab="y1")title(main="", cex=0.8)

## Compute solution manually for y2 at t=10 and compare with simulated solutiont=10evecs_norm[2,1]*c[1,1]*evals[1]^t+evecs_norm[2,2]*c[2,1]*evals[2]^t# analytical solution

# Compare y2/y1 with normalised dominant eigenvectory2_y1[,Q]

[1] 0.3333333

evecs_norm[2,1]

[1] 0.3333333

NotePython code

import matplotlib.pyplot as plt# Set the number of periods for simulationQ =100# Initialize arrays to store values for different periodsy1 = np.ones(Q)y2 = np.ones(Q)# Solve the system recursively based on the initializationfor t inrange(1, Q): y1[t] = J[0, 0] * y1[t -1] + J[0, 1] * y2[t -1] y2[t] = J[1, 0] * y1[t -1] + J[1, 1] * y2[t -1]# Plot dynamics of y1plt.plot(range(Q), y1, color='b', linewidth=2)plt.xlabel('Time')plt.ylabel('y1')plt.title('Dynamics of y1')plt.show()# Define the initial conditions y0y0 = np.array([y1[0], y2[0]])# Calculate the arbitrary constants c using the normalized eigenvectorsc = np.linalg.inv(evecs_norm).dot(y0)c## Compute solution manually for y2 at t=10 and compare with simulated solutiont =10evecs_norm[1, 0] * c[0] * evals[0] ** t + evecs_norm[1, 1] * c[1] * evals[1] ** ty2[t]# Calculate the ratio y2/y1y2_y1 = y2 / y1# Plot dynamics of y2/y1 for the first 50 periodsplt.plot(y2_y1[:50], color='black', linewidth=2, linestyle='-')plt.xlabel('Time')plt.ylabel('y2/y1')plt.show()# Compare y2/y1 with normalised dominant eigenvectory2_y1[Q-1]evecs_norm[1,0]

It can be seen that the simulated results are equivalent to the results we obtained analytically. The key takeaway is that by deriving information about the eigenvalues (and possibly eigenvectors) of the coefficient matrix of the system, we are able to deduce knowledge of the dynamic properties of the system even without numerical simulation. However, the more complex the dynamic system, the more difficult this will be, thereby rendering numerical simulation a key tool to supplement formal analysis.

An economic example: Samuelson’s (1939) multiplier accelerator model

Consider the multiplier accelerator model by Samuelson (1939) discussed in Chapter 2:

Assuming \(c_1=0.8\) and \(\beta=0.3\), we can compute the eigenvalues:

# Set fixed parameter valuesc1=0.8beta=0.3## Compute eigenvalues# Define coefficient matrixA=matrix(c(c1, c1,beta*(c1-1), beta*c1), 2, 2, byrow=TRUE)# Obtain eigenvalues and eigenvectorsev=eigen(A)(evals=ev$values)

[1] 0.694356 0.345644

NotePython code

# Set parameter valuesc1 =0.8beta =0.3# Define the coefficient matrixA = np.array([[c1, c1], [beta * (c1 -1), beta * c1]])# Calculate eigenvalues and eigenvectorsevals, evecs = np.linalg.eig(A)print(evals)print(evals)

and conclude that since the dominant eigenvalue is smaller than one (in absolute terms), the system is stable.

Complex eigenvalues and cycles

So far, we have discussed the case where the eigenvalues \(\lambda\) are real numbers. However, what if the polynomial \(det(A-\lambda I)=0\) does not yield real numbers? Recall that in the case of a second-order polynomial \(\lambda^2+b\lambda+c=0\), the two roots are given by \(\lambda_{1,2} = \frac{-b \pm \sqrt{b^2-4c}}{2}\). If the term under the root \(\Delta=b^2-4c\), also called discriminant, becomes negative, the solution will be a complex number. More specifically, we can write:

The two eigenvalues will be a pair of complex conjugates if \([c_1(1+\beta)]^2-4\beta c_1 <0\) or \(c_1 < \frac{4\beta}{(1+\beta)^2}\).

Suppose we have \(c_1=0.4\) and \(\beta=2\). Then the discriminant will be negative and the eigenvalues will be complex:

#Clear the environment rm(list=ls(all=TRUE))# Set parameter valuesc1=0.4beta=2# Check if discriminant is negative(c1*(1+beta))^2-4*c1*beta

[1] -1.76

## Find eigenvalues and eigenvectors of matrix# Define matrixA=matrix(c(c1, c1,beta*(c1-1), beta*c1), 2, 2, byrow=TRUE)# Obtain eigenvalues and eigenvectorsev=eigen(A)(evals=ev$values)

[1] 0.6+0.663325i 0.6-0.663325i

NotePython code

# Set parameter valuesc1 =0.4beta =2# Check if discriminant is negative(c1 * (1+ beta))**2-4* c1 * beta# Define the matrixA = np.array([[c1, c1], [beta * (c1 -1), beta * c1]])# Calculate eigenvalues and eigenvectorsevals, evecs = np.linalg.eig(A)print(evals)print(evals)

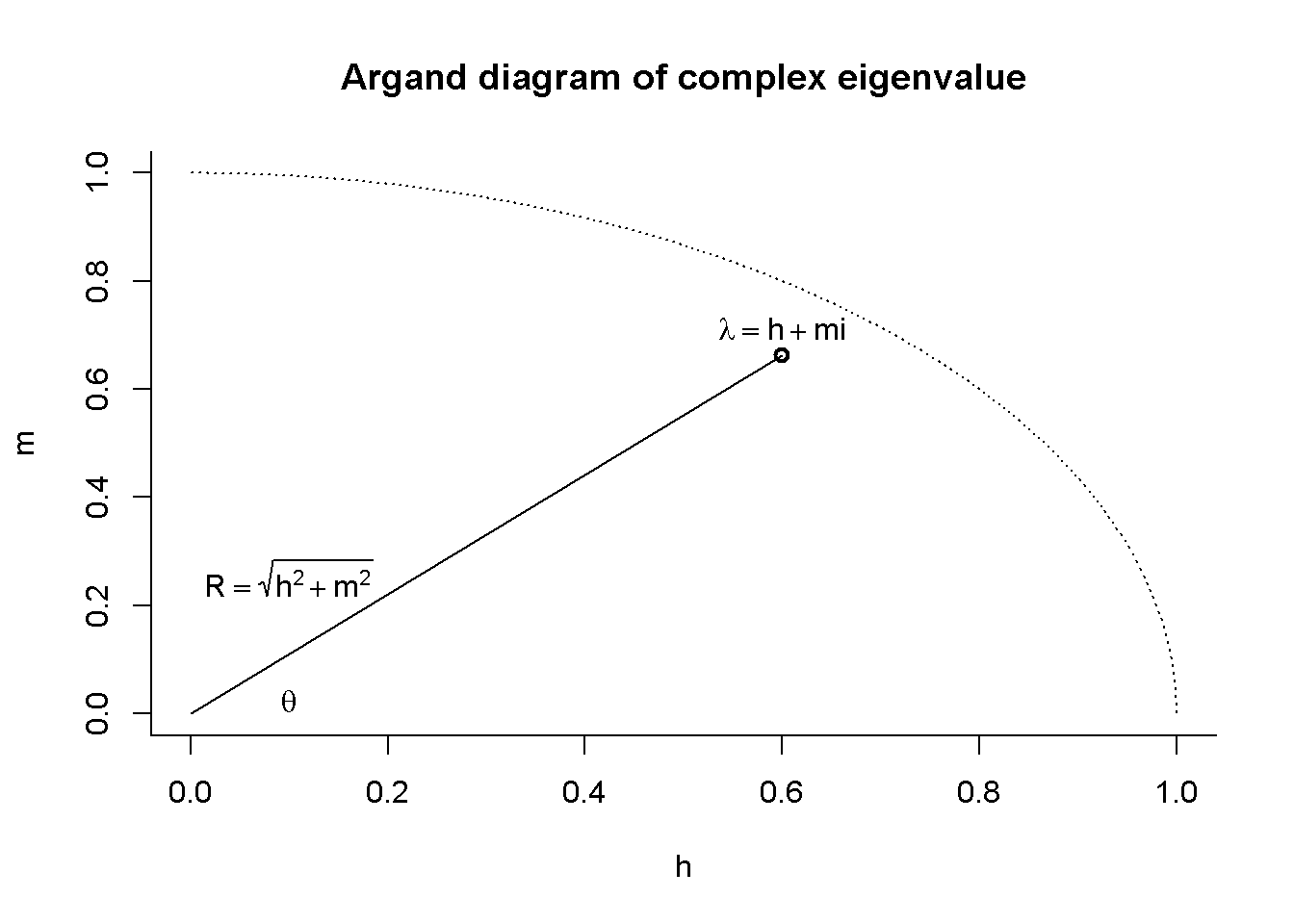

Another way of understanding the logic behind complex numbers is through a so-called Argand diagram that plots the real part of the eigenvalue on the horizontal and the imaginary part on the vertical axis. By Pythagoras’ theorem, the distance of the eigenvalue from the origin will then be given by \(R=\sqrt{h^2+m^2}\). The value of \(R\) (which is always real-valued and positive) is called the modulus (or absolute value) of the complex eigenvalue and will contain important information about the dynamic stability of economic models that exhibit complex eigenvalues.

### Draw Argand diagram# Save real and imaginary part of complex eigenvaluere=Re(evals[1])im=Im(evals[1])# Plot complex eigenvaluepar(bty="l")plot(re,im, type="o", xlim=c(0, 1), ylim=c(0, 1), lwd=2, xlab="h", ylab="m", main="Argand diagram of complex eigenvalue")# Plot unit circleX=seq(0, 1, by=0.001)Y=sqrt(1-X^2)lines(X,Y, type="l", lty="dotted")# Plot a ray from the origin to eigenvaluesegments(0,0,re,im, lty='solid')# Add labelstext(0.1, 0.025, expression(theta), cex=1)text(0.1, 0.25, expression(R==sqrt(h^2+m^2)), cex=1)text(re, im+0.05, expression(lambda==h+mi), cex=1)

NotePython code

### Draw Argand diagram# Save real and imaginary part of complex eigenvaluere = evals[0].realim = evals[0].imag# Create a figurefig, ax = plt.subplots()ax.set_xlim(0, 1)ax.set_ylim(0, 1)ax.set_xlabel('h')ax.set_ylabel('m')ax.set_title('Argand diagram of complex eigenvalue')# Plot complex eigenvalueax.plot(re, im, 'o', markersize=8, color='k')# Plot unit circleX = np.linspace(0, 1, 100)Y= np.sqrt(1-X**2)ax.plot(X, Y, 'k--')# Plot a ray from the origin to the eigenvalueax.plot([0, re], [0, im], 'k-')# Add labelsax.text(0.1, 0.025, r'$\theta$', fontsize=12)ax.text(0.001, 0.25, r'$R=\sqrt{h^2+m^2}$', fontsize=12)ax.text(re, im -0.1, r'$\lambda=h+mi$', fontsize=12)plt.show()

The angle \(\theta\) of the line that connects the origin and the complex eigenvalue and the x-axis of the Argand diagram also contains information about the dynamics. To see this, note that the geometry of the complex number represented in the Argand diagram can also be expressed in trigonometric form: \[

\sin\theta=\frac{m}{R}

\]\[

\cos\theta=\frac{h}{R},

\]

where \(\theta=\arcsin (\frac{m}{R}) =\arccos (\frac{h}{R})=\arctan(\frac{m}{h})\)

Thus, we can write the complex eigenvalue also as:

By De Moivre’s theorem, we have \((\cos\theta \pm \sin\theta \times i)^t=(\cos\theta t \pm \sin\theta t \times i)\). Thus, the solution to a dynamic system that exhibits complex eigenvalues will be of the form:

\[

y_{1t}=v_{11}c_1 R_1^t(\cos\theta_1 t \pm \sin\theta_1 t \times i) +...+ y^*_1.

\]

From this solution we can again deduce key information about the dynamics of the system based on the (complex) eigenvalues:

stability will depend on the modulus: for \(R<1\) the system will be stable, for \(R>1\) it will be unstable

from the nature of the trigonometric functions \(\sin(\theta t)\) and \(\cos(\theta t)\), we know that system will exhibit periodic cyclical dynamics as \(t\) increases

the length of the cycles will be given by \(L=\frac{2\pi}{\theta}\) and the frequency by \(F=1/L=\frac{\theta}{2\pi}\)

the amplitude of the cycles will depend on the elements of the eigenvectors, the initial conditions, and \(R\).

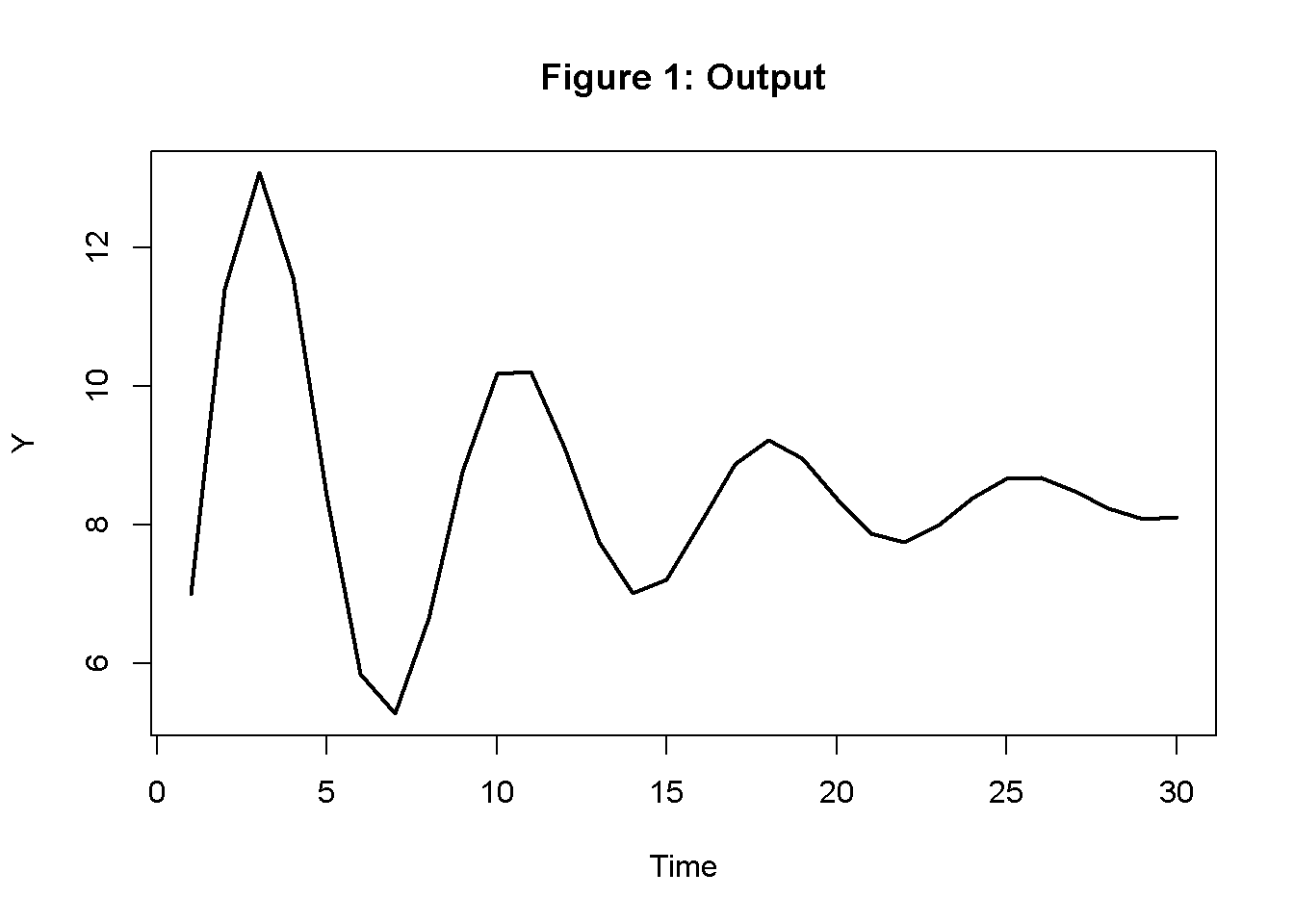

Let us simulate the Samuelson model with the parameterisation that yields complex eigenvalues to illustrate these results:

# Set number of periods for which you want to simulateQ=100# Set number of parameterisations that will be consideredS=1# Construct matrices in which values for different periods will be stored; initialise at 1C=matrix(data=1, nrow=S, ncol=Q)I=matrix(data=1, nrow=S, ncol=Q)#Construct matrices for exogenous variableG0=matrix(data=5, nrow=S, ncol=Q)#Solve this system recursively based on the initialisationfor(tin2:Q){C[1,t]=c1*(C[1,t-1]+I[1,t-1]+G0[1,t])I[1,t]=beta*(c1*(C[1,t-1]+I[1,t-1]+G0[1,t])-C[1,t-1])}# close t1me loop# Calculate outputY=C+G0+I# Time series chart of output dynamics in Samuelson (1939) modelplot(Y[1, 1:30],type="l", col=1, lwd=2, lty=1, xlab="Time", ylab="Y")title(main="Output fluctuations in Samuelson model with complex eigenvalues", cex=0.8)

NotePython code

# Calculate modulusmod =abs(evals[0])print(mod)# Calculate cycle lengthimport mathL = (2* math.pi) / math.acos(re / mod)print(L)# Set the number of periods and parameterizationsQ =100S =1# Initialize matrices for consumption, investment, and exogenous government spendingC = np.ones((S, Q))I = np.ones((S, Q))G0 = np.full((S, Q), 5)# Solve the system recursively based on the initializationfor t inrange(1, Q): C[0, t] = c1 * (C[0, t -1] + I[0, t -1] + G0[0, t]) I[0, t] = beta * (c1 * (C[0, t -1] + I[0, t -1] + G0[0, t]) - C[0, t -1])# Calculate outputY = C + G0 + I# Plot the time series chart of output dynamicsplt.plot(Y[0, :30], color='k', linewidth=2, linestyle='-')plt.xlabel("Time")plt.ylabel("Y")plt.title("Output fluctuations in Samuelson model with complex eigenvalues")plt.show()

You can see that the model generates cycles with a length (from peak/trough to peak/trough) of around 7.5 periods. Since the modulus is \(R<1\), the system is stable and eventually converges to the equilibrium. This type of cyclical dynamics is called damped oscillations.

A general condition for stability of 2D systems with complex eigenvalues can be derived by making use of the fact that \(R=\sqrt{h^2+m^2}= \sqrt{ \left( \frac{b}{2} \right) ^2 + \left(\frac{\sqrt{4c-b^2}}{2} \right)^2} = \sqrt{c}\), where \(b=tr(J)\) and \(c=det(J)\).

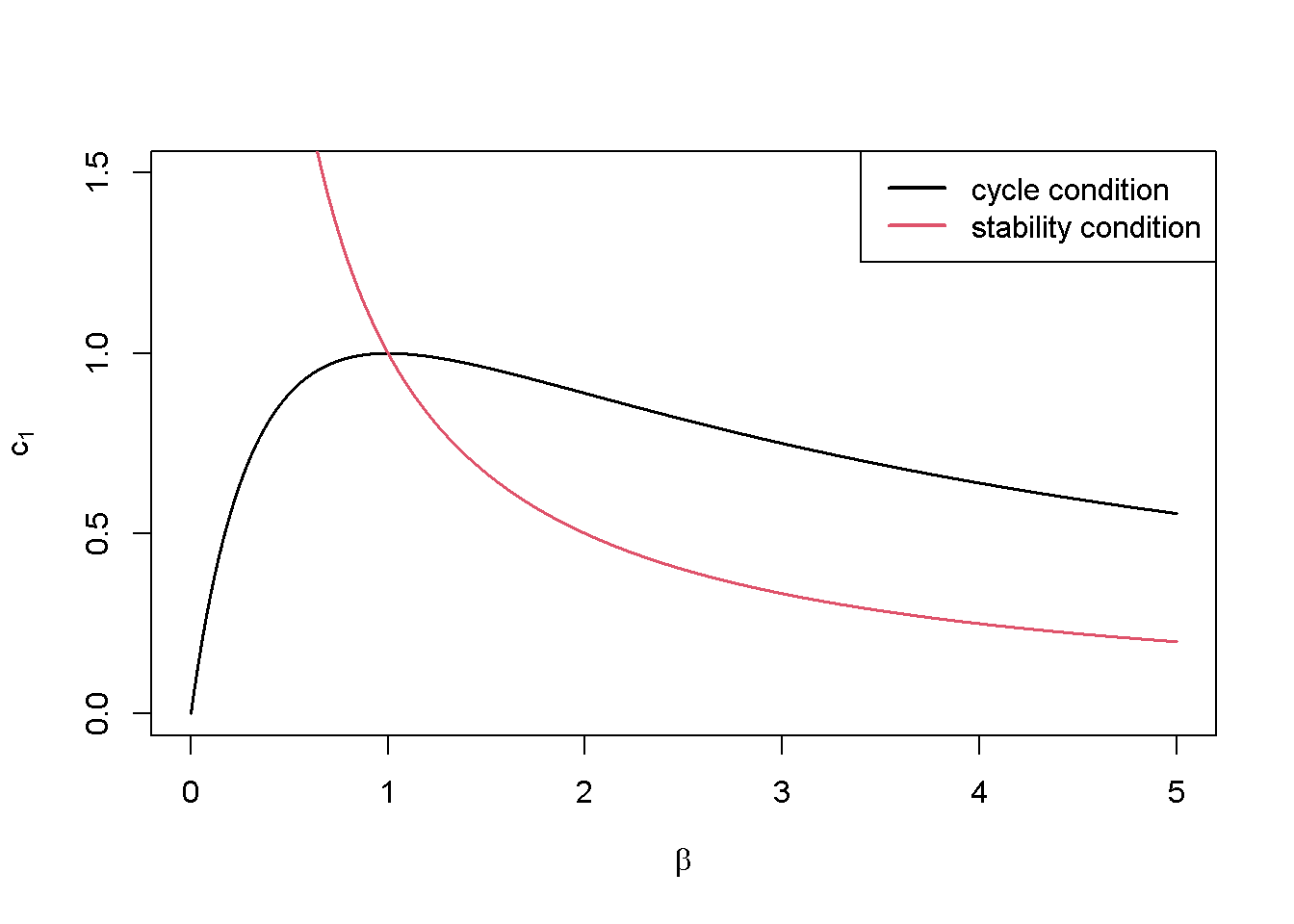

Applied to the modulus of the Samuelson model, this yields \(R=\sqrt{det(J)}=\sqrt{\beta c_1}\). Thus, the stability condition is:

\[\beta c_1<1.\]

The following code generates a plot that displays the condition for cycles and the stability condition in the \((\beta, c_1)\)-space:

# Create function for cycle condition: c1 < (4*beta)/(1+beta)^2cyc=function(beta){(4*beta)/(1+beta)^2}# Create function for stability condition: c1 < 1/betastab=function(beta){1/beta}# Plot the two functions in (beta, c1)-spacecurve(cyc, from =0, to =5, col =1, xlab=expression(beta), ylab=expression(c[1]) , main="", lwd=1.5, n=10000, ylim=range(0, 1.5))curve(stab, from =0, to =5, col =2, lwd=1.5, n=10000, add =TRUE)legend("topright", legend =c("cycle condition", "stability condition"), col =c(1, 2), lwd =2)

NotePython code

import numpy as npimport matplotlib.pyplot as plt# Create function for cycle condition using beta as argumentdef cyc(beta):return (4* beta) / (1+ beta)**2# Create function for stability condition using beta as argumentdef stab(beta):return1/ beta# Define the range of beta valuesbeta = np.linspace(0.001, 5, 10000) # start from 0.001 to avoid division by zero# Plot the two functions in (beta, c1)-spaceplt.plot(beta, cyc(beta), label="cycle condition", color='black', linewidth=1.5)plt.plot(beta, stab(beta), label="stability condition", color='red', linewidth=1.5)# Set labels and titleplt.xlabel(r'$\beta$')plt.ylabel(r'$c_1$')plt.ylim(0, 2)plt.legend(loc="upper right")# Display the plotplt.show()

Combinations of \(c_1\) and \(\beta\) below the cycle condition curve yield complex eigenvalues and thus cycles, while combinations below the stability condition curve yield an asymptotically stable equilibrium.

Nonlinear systems

So far, we have analysed dynamic systems that are linear. However, in the more general case, a dynamic system may be nonlinear and of the form:

\[

y_t=f(y_{t-1}).

\]

An \(n\)-dimensional nonlinear system may have multiple equilibria \(y^*\). To analyse the dynamic properties of such a system, we normally conduct a linear approximation in the neighbourhood of one of the equilibria. In that sense, the stability analysis of a nonlinear system has only local as opposed to global validity.

Mathematically, linearisation around an equilibrium point can be done by conducting a first-order Taylor expansion around that equilibrium:

This yields a linear version of the system that can be written as:

\[

y_{t}=Ay_{t-1}+B,

\]

where \(A_{11}=\frac{\partial f^1(y^*)}{\partial y_{1t-1}}\) and so forth.

The matrix \(A\) is the so-called Jacobian matrix of the system \(f(y_{t-1})\)evaluated at\(y^*\). The Jacobian matrix collects all partial derivatives of the state variables \(y_t\) with respect to each other, i.e. \(\frac{\partial y_{1t}}{\partial y_{1t-1}}\), \(\frac{\partial y_{1t}}{\partial y_{2t-1}}\), and so on.3 The linearised Jacobian matrix \(A\) can be obtained by plugging the equilibrium solutions for \(y^*\) into the Jacobian.

In practice, this means that to analyse the local stability of a nonlinear system, one needs to:

find the equilibrium solution \(y^*\) whose neighbourhood you want to analyse

compute the Jacobian matrix of \(f(y_{t-1})\)

substitute \(y^*\) into the Jacobian and analyse the resulting matrix.

An example for the stability analysis of a simple two-dimensional nonlinear system can be found in Section 11.5.

From an modelling point of view, nonlinear dynamic systems are of considerable interest because they allow for richer dynamics. For example, under certain conditions, a nonlinear system with complex eigenvalues can generate a limit cycle, which is an endogenous cycle that continues indefinitely without external shocks. A second example are chaotic dynamics, which are seemingly random despite being generate by a deterministic system. Chaotic models also often displayed sensitivity to initial conditions, i.e. a form of path dependence.

Key takeaways

dynamic models are systems of difference (or differential) equations

the stability of a system depends on (a combination of) its coefficients

more generally, the system’s dynamic properties (including stability) are encapsulated in the Jacobian matrix

the dominant eigenvalue \(\lambda\) (or modulus in the case of complex eigenvalues) of the Jacobian matrix indicates whether a system is

stable (\(|\lambda| < 1\)) or unstable (\(|\lambda| > 1\))

acyclical (\(\lambda \in \mathbb{R}\)) or cyclical (\(\lambda \in \mathbb{C}\))

the (dominant) eigenvectors mediate the impact of the eigenvalues on the dynamics

nonlinear systems are analysed locally around one of their equilibria

A simplified recipe for analysing dynamic systems

Identify the state variables of your model, i.e. \(y_t = f(y_{t-1})\)

Substitute away any other endogenous variables that are not state variables (e.g. by using the equilibrium solutions of the endogenous variables that are determined simultaneously within every period)

Write your model as a system in the state variables only (with otherwise only exogenous parameters/variables)

Find the steady state solutions to the state variables by setting \(y_t = y_{t-1}=y^*\)

Construct the Jacobian matrix of the system containing the partial derivatives of the state variables with respect to each other

If the model has nonlinearities, plug the steady state solutions into the Jacobian matrix

Check the stability of the system by relying on well-known stability conditions, e.g. those in Gandolfo (2009)

Check if other interesting properties can be derived (e.g. complex eigenvalues)

Confirm your analytical results through numerical simulations, e.g. compute the eigenvalues, check the stability conditions, etc.

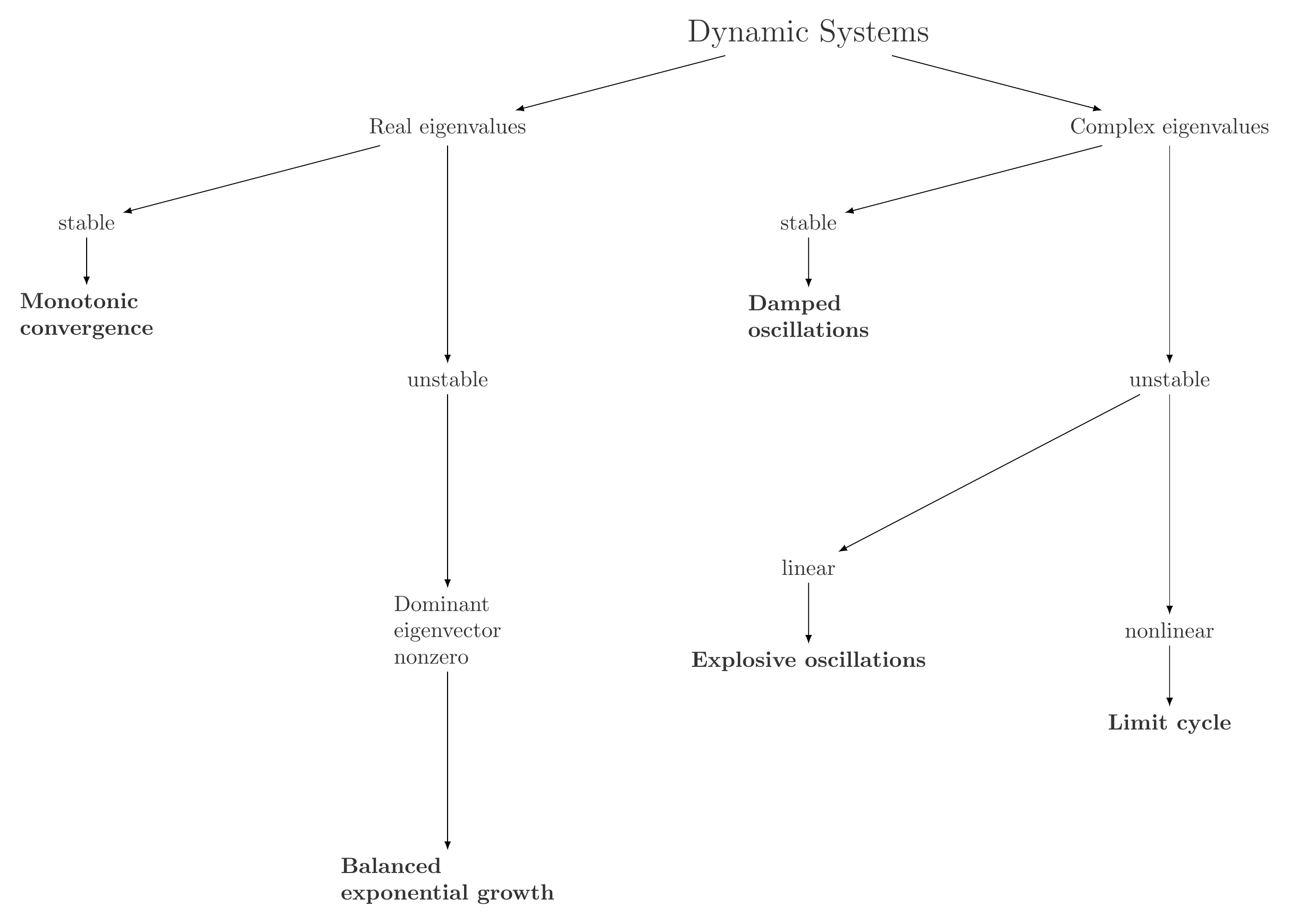

A typology of dynamic systems

The following typology classifies dynamic systems based on their eigenvalues, which give rise to different dynamic properties, as explained in this section.

A typology of dynamic systems

In this section, we analysed the linear Samuelson (1939) model and showed that it can give rise to either monotonic convergence (if its eigenvalues are real) or damped oscillations (if they are complex). Exponential growth and explosive oscillations are also possible, if the model becomes unstable.

Based on this typology, we can classify the dynamic models on this website as follows:

Anthony, Martin, and Michele Harvey. 2012. Linear Algebra: Concepts and Methods. Cambridge University Press.

Chiang, Alpha C, and Kevin Wainwright. 2005. Fundamental Methods of Mathematical Economics. 4th ed. McGraw-Hill Education.

Gandolfo, Giancarlo. 2009. Economic Dynamics. Study Edition. 4th Edition. Springer.

Samuelson, Paul A. 1939. “Interactions between the Multiplier Analysis and the Principle of Acceleration.”The Review of Economics and Statistics 21 (2): 75–78. https://doi.org/10.2307/1927758.

Sayama, Hiroki. 2015. Introduction to the Modeling and Analysis of Complex Systems. Open SUNY Textbooks, Milne Library.

We will focus here on difference instead of differential equations, i.e. on dynamics in discrete as opposed to continuous time. Most of the continuous-time counterpart is analogous to the material covered here. Sayama (2015) provides a very accessible and applied introduction to dynamic systems with Python code. An introductory treatment of the underlying mathematics is Chiang and Wainwright (2005), chaps. 15-19. Gandolfo (2009) provides a more advanced treatment of the mathematics as well as many economic examples. A great introduction to linear algebra is Anthony and Harvey (2012).↩︎

This is because in the product \((PDP^{-1})(PDP^{-1})(PDP^{-1})...\), each \(P\) cancels a \(P^{-1}\), except for the first \(P\) and last \(P^{-1}\).↩︎

In this way, the Jacobian matrix can be regarded as a more general version of the coefficient matrix in linear systems.↩︎