This section provides a general introduction into the simulation of economic models. It finishes with a little exercise that will help you build the skills to simulate and visualise models yourself.

Introduction: economic models

Why do we build formal economic models? Because they help us think carefully about the causal mechanisms that generate certain economic outcomes (e.g. unemployment). Models are especially useful when the variables of interest are inherently quantitative (e.g. the interest rate and unemployment) and when several of these quantitative variables interact with each other. More specifically, models provide a precise formal representation of a set of interlinked causal mechanisms that are often difficult to analyse informally.

Every economic model essentially consists of three things:

a set of \(N\) equations

a set of \(N\) endogenous variables

a set of exogenous or fixed coefficients (‘parameters’) and exogenous variables

The solution to the model, its ‘equilibrium’, will pin down values for the endogenous variables of the model for a given set of parameters and exogenous variables. Thus, the endogenous variables, e.g. unemployment, are determined within the system, while exogenous variables are determined outside of the system and often reflect policy variables, such as the central bank interest rate or government spending. The equations connect the variables of the system. They typically express:

economic (accounting) identities (e.g. that in a closed economy without government, saving is income that is not consumed: \(S=Y-C\))

budget constraints (e.g. that business investment can be financed out of retained profits and new debt, \(I=\Pi+\Delta D\))

behavioural functions (e.g. that households consume a constant proportion of their income, \(C=c_1Y\)), which often contain key parameters of the model (e.g. the marginal propensity to consume \(c_1\))

equilibrium conditions (e.g. that demand must be equal to supply)

Equations may be linear or nonlinear. If a model contains nonlinear relationships between the endogenous variables, it may admit more than one solution (often called multiple equilibria).

Economic models can be either static or dynamic. In a static model, time plays no role and all endogenous variables are determined simultaneously. In a dynamic model, time matters and the endogenous variables adjust gradually over time.

The endogenous variables are typically interrelated: e.g. \(x\) determines \(y\), but \(y\) also determines \(x\). These interrelationships can be:

simultaneous: \(x\) and \(y\) determine each other simultaneously (within the same period)

recursive: \(x\) affects \(y\) only in \(t+1\) (or vice versa)

Unlike static models, dynamic models describe what happens out of equilibrium.1 Note that dynamic models may contain both simultaneous and recursive relationships.

Whether the relationships between the variables is simultaneous or recursive has implications for how the model can be solved. In general, simple economic models can often be solved analytically without a computer. If the model contains simultaneous relationships, it needs to be solved as a simultaneous system by solving for the endogenous variables through repeated substitution. This means going from the so-called ‘structural form’, i.e. the full set of equations, to the so-called ‘reduced form’, where the right-hand side of the equations only contains exogenous variables and parameters. If the system is linear, techniques from linear algebra such as matrix inversion or Cramer’s rule can be used (see Chiang and Wainwright (2005), chaps. 4-5). If the system contains recursive relationships, the equilibrium solution can be found by setting \(x_{t+i}=x_{t-i}=x_{t}\) for all \(x\) and then solving the resulting simultaneous system (more on this Chapter 9).

However, often a complete analytical solution is difficult to come by. Common challenges are:

a model has more than 3 dimensions (\(N>3\)): then it’s very tedious to compute analytical solutions

a model has nonlinearities that preclude the computation of analytical solutions

a model is dynamic and you want to examine the dynamic adjustment of the endogenous variables (which is tedious to do analytically)

In these cases, numerical solution by means of computer simulation becomes useful. A key advantage is that it allows you to study much more complex models than the analytical approach does. A key disadvantage is that numerical solution requires the choice of a (possibly arbitrary) set of numerical values for the models’ parameters. It is thus less general than analytical solution – a limitation which should be borne in mind. We think that both analytical and numerical approaches are useful. Correspondingly, we supplement the numerical simulations with analytical model solutions where possible.

Solving economic models numerically

If a (dynamic) model exclusively contains recursive relationships, it can be solved iteratively by sequentially updating the endogenous variables from (arbitrarily set) initial conditions. This is easy to do with a computer. By contrast, if interrelationships are simultaneous, solving the system for the endogenous variables as described above is less trivial for a computer (finding the solution for \(x\) requires the solution of \(y\), but the latter requires in turn the solution for \(x\)). One approach is to use linear algebra: cast the system in matrix form (\(b=Ax\)) and let the computer find \(x^*=A^{-1}b\) through some algorithm (e.g. the Gauss-Seidel method).

We will use an approach that is simpler and based on iteration:

choose a set of numerical parameter values (e.g. a marginal propensity to consume of \(c_1=0.8\))

choose (arbitrary but non-zero) initial values for the endogenous variables (e.g. \(C=Y=1)\)

then solve the system of equations many times using a for loop

In this way, the solution gets approximated successively.

A limitation of the method of iteration is that it will only converge to the solution of the simultaneous component of a model if the equilibrium is stable (more on stability in Chapter 9). For most static models, stability is required for the model to be economically meaningful. In that sense, if the iterative approach does not yield a solution, this is a sign that the model and/or parameterisation needs to be reconsidered. In dynamic models, stability is a key question that should be addressed in any case. Therefore, this limitation of the method of iteration may not be too restrictive in practice.

Solving economic models numerically: examples

A static model

Consider a two-dimensional simultaneous system represented by a simple Keynesian goods market model. We can use this model to make a theoretical prediction of how an increase in government spending affects aggregate output.

\[

Y= C + G_0

\]\[

C = c_0 + c_1Y

\]

Aggregate demand is composed of consumption \(C\) and government spending \(G_0\). The latter is assumed to be exogenous and will be treated as a causal driver of changes in aggregate income and consumption. Goods market equilibrium requires aggregate demand to be equal to aggregate income \(Y\) (first equation). Consumption is assumed to be determined by an autonomous component \(c_0\) and a marginal propensity to consume out of income \(c_1\) (second equation).

Through the method of substitution, we can easily derive the analytical solution for equilibrium output: \(Y^*=\frac{c_0+G_0}{1-c_1}\). With this solution, we can work out the predicted effect of an increase in government spending on output: \(\frac{\partial Y^*}{\partial G_0}=\frac{1}{1-c_1}\).

We are interested in how an increase in government spending from \(G_0=5\) to \(G_0=6\) affects the solution of the system, especially equilibrium output. To solve the model numerically, suppose the parameters of the consumption function are given by \(c_0=3\) and \(c_1=0.8\). The code below shows how to find the solution via simulation.

### Simulate Keynesian goods market model via iteration#Clear the environment rm(list=ls(all=TRUE))# Set number of parameterisations that will be consideredS=2# Set fixed parameter valuesc0=3c1=0.8#Create vector in which equilibrium solutions from different parameterisations will be storedY_eq=vector(length=S)C_eq=vector(length=S)#Create vector with exogenous value for government spending that will change across scenarios G0=vector(length=S)G0[1]=5G0[2]=6# Initialise endogenous variables at arbitrary positive value Y=C=1#Solve this system numerically through 1000 iterations based on the initialisationfor(iin1:S){for(iterationin1:1000){Y=C+G0[i]C=c0+c1*Y}# close iterations loop#Save results for different parameterisations in vectorY_eq[i]=YC_eq[i]=C}# close parameterisations loop# Display solutionsY_eq

[1] 40 45

C_eq

[1] 35 39

# Verify solutions for Y using the analytical solution (c0+G0[])/(1-c1)

[1] 40 45

NotePython code

### Simulate Keynesian goods market model via iteration# Load NumPy libraryimport numpy as np# Set the number of parameterisations that will be consideredS =2# Set fixed parameter valuesc0 =3c1 =0.8# Create numpy arrays in which equilibrium solutions from different parameterisations will be storedY_eq = np.zeros(S)C_eq = np.zeros(S)#Create vector with exogenous value for government spending that will change across scenarios G0 = np.zeros(S)G0[0] =5G0[1] =6# Initialize endogenous variables at an arbitrary positive valueY = C =1# Solve this system numerically through 1000 iterations based on the initializationfor i inrange(S):for iteration inrange(1000): Y = C + G0[i] C = c0 + c1 * Y# Save results for different parameterisations in the numpy arrays Y_eq[i] = Y C_eq[i] = C# Display solutions for YY_eq# Verify solutions for Y using the analytical solution (c0+G0)/(1-c1)

Let’s break this code down:

set the number of scenarios \(S\), define parameter values, and create vectors of length \(S\) in which the results for the endogenous variables will be stored

define changes in exogenous variables or parameters (i.e. construct different scenarios)

initialise the endogenous variables

write down the equations (solved for the endogenous variables such that every endogenous variable of the system appears on the left-hand side of an equation exactly once)

place these equations inside a for loop

the loop says: repeat the segment of code inside the curly brackets 1000 times

nest the loop that solves the system in an outer loop that loops through different parameterisations (here for different values of \(G_0\))

after the iterations loop is finished, save the results for the current parameterisation

What happens is the following: in the first iteration, \(Y\) and \(C\) are calculated based on the initial values and the parameter values. In the second iteration, the values are then overwritten based on the results from the first iteration. This process continues 1000 times. In this way, the correct solution is successively approximated. If you have an analytical solution, you can compare it with the numerical one to double-check your results.

When does the method of iteration fail to provide a solution? In the following code, everything is the same with the only difference that the marginal propensity to consume is now larger than unity (\(c_1=1.2\)). Now the numerical simulation fails to find the correct solution. This is because with \(c_1>1\), the so-called Keynesian equilibrium condition is violated and the equilibrium happens to be unstable. We will discuss in Chapter 9 the issue of stability and how to analyse it formally. At this point, we simply note that the method of iterations requires static models to be stable to yield equilibrium solutions.

### Parameterisation for which method of iteration fails#Clear the environment rm(list=ls(all=TRUE))# Set number of parameterisations that will be consideredS=2# Set fixed parameter valuesc0=3c1=1.2#Create vector in which equilibrium solutions from different parameterisations will be storedY_eq=vector(length=S)C_eq=vector(length=S)#Create vector with parameter that will change G0=vector(length=S)G0[1]=5G0[2]=6# Initialise endogenous variables at arbitrary positive value Y=C=1#Solve this system numerically through 1000 iterations based on the initialisationfor(iin1:S){for(iterationin1:1000){Y=C+G0[i]C=c0+c1*Y}# close iterations loop#Save results for different parameterisations in vectorY_eq[i]=YC_eq[i]=C}# close parameterisations loop# Display solutionY_eq

[1] 5.818655e+80 8.832196e+159

# Verify solutions for Y(c0+G0[])/(1-c1)

[1] -40 -45

NotePython code

### Parameterisation for which method of iteration failsc1 =1.2# Initialize endogenous variables at an arbitrary positive valueY = C =1# Solve this system numerically through 1000 iterations based on the initializationfor i inrange(S):for iteration inrange(1000): Y = C + G0[i] C = c0 + c1 * Y# Save results for different parameterisations in the numpy arrays Y_eq[i] = Y C_eq[i] = C# Display solutions for Y_eqY_eq# Verify solutions for Y(c0+G0)/(1-c1)

A dynamic model (in discrete time)

Consider now a dynamic version of the Keynesian goods market model that was proposed by Paul Samuelson (1939). In this model, investment (\(I\)) is endogenous and reacts to the change in consumption. Consumption (\(C\)) responds to changes in income (\(Y\)) with a lag:

\[

Y_t = C_t + I_t + G_0

\]\[

I_t = \beta(C_t - C_{t-1})

\]\[

C_t=c_1Y_{t-1}.

\] This is a dynamic model, in which the endogenous variables adjust gradually over time. However, the model is not purely recursive as investment reacts to consumption in the same period (and output to consumption and investment). By shifting \(Y_t=C_t + I_t + G_0\) one period back, substitution into the consumption, and then investment function, the system can be reduced to two equations that are fully recursive:

\[

C_t= c_1(C_{t-1} + I_{t-1} + G_0)

\]\[

I_t= \beta[c_1(C_{t-1} + I_{t-1} + G_0) - C_{t-1}]

\] We can find the solution for output analytically by setting \(x_t=x_{t-1}\) for all variables and then applying the method of substitution. This yields \(Y^*=\frac{G_0}{1-c_1}\). The code below shows how to find this solution through simulation.

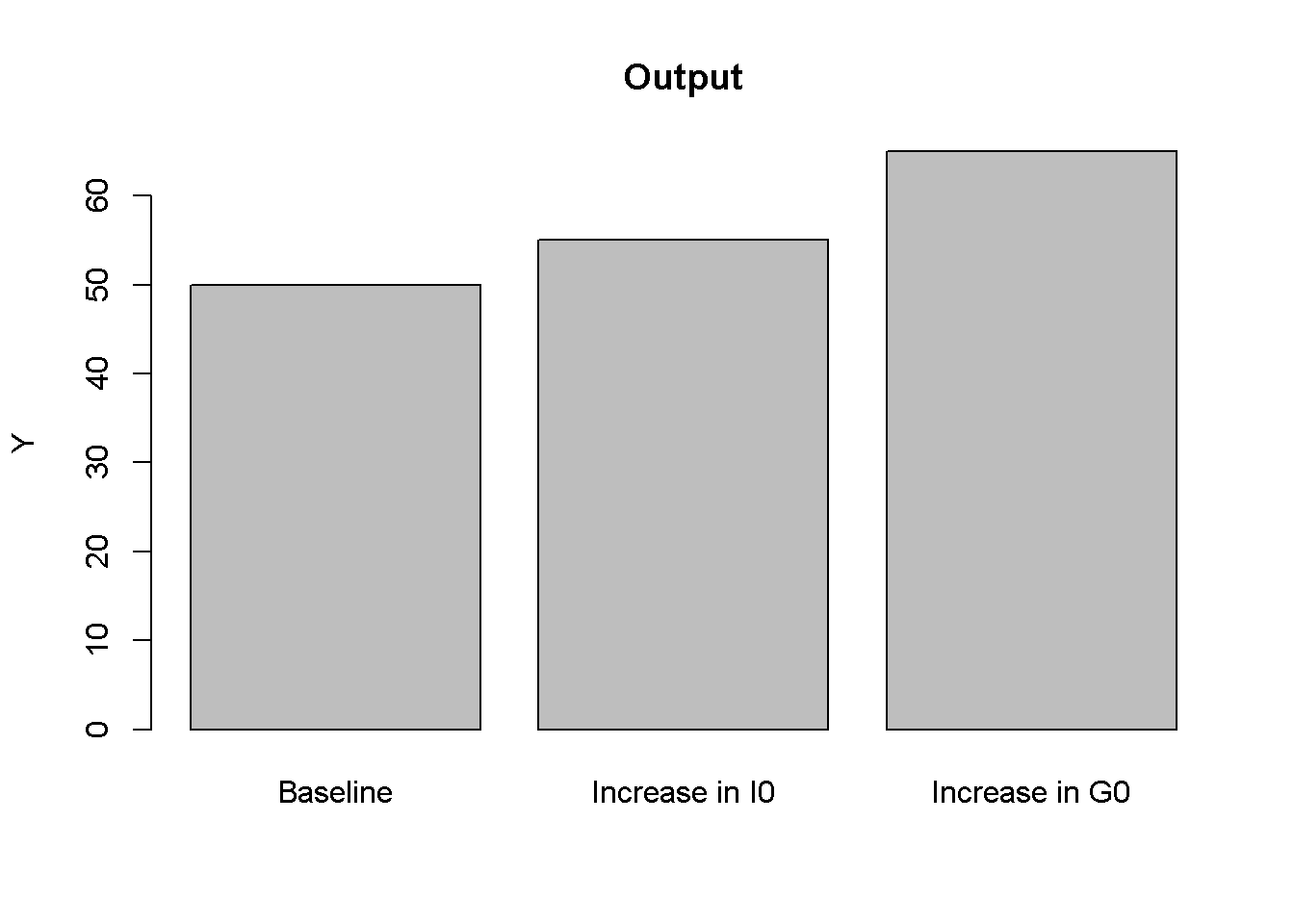

### Simulate Samuelson 1939#Clear the environment rm(list=ls(all=TRUE))# Set number of periods for which you want to simulateQ=100# Set number of parameterisations that will be consideredS=2# Set period in which shock or shift will occurs=15# Set fixed parameter valuesc1=0.8beta=0.6# Construct (S x Q) matrices in which values for different periods will be stored; initialise at 1C=matrix(data=1, nrow=S, ncol=Q)I=matrix(data=1, nrow=S, ncol=Q)#Construct matrices for exogenous variable or parameter that will change over time to capture different scenariosG0=matrix(data=5, nrow=S, ncol=Q)# Set parameter values for different scenariosG0[2,s:Q]=6# scenario: permanent increase in government spending from G0=5 to G0=6 from period s=15 onwards#Solve this system recursively based on the initialisationfor(iin1:S){for(tin2:Q){C[i,t]=c1*(C[i,t-1]+I[i,t-1]+G0[i,t])I[i,t]=beta*(c1*(C[i,t-1]+I[i,t-1]+G0[i,t])-C[i,t-1])}# close time loop}# close scenarios loop# Calculate outputY=C+G0+I# Display solutionY[,Q]

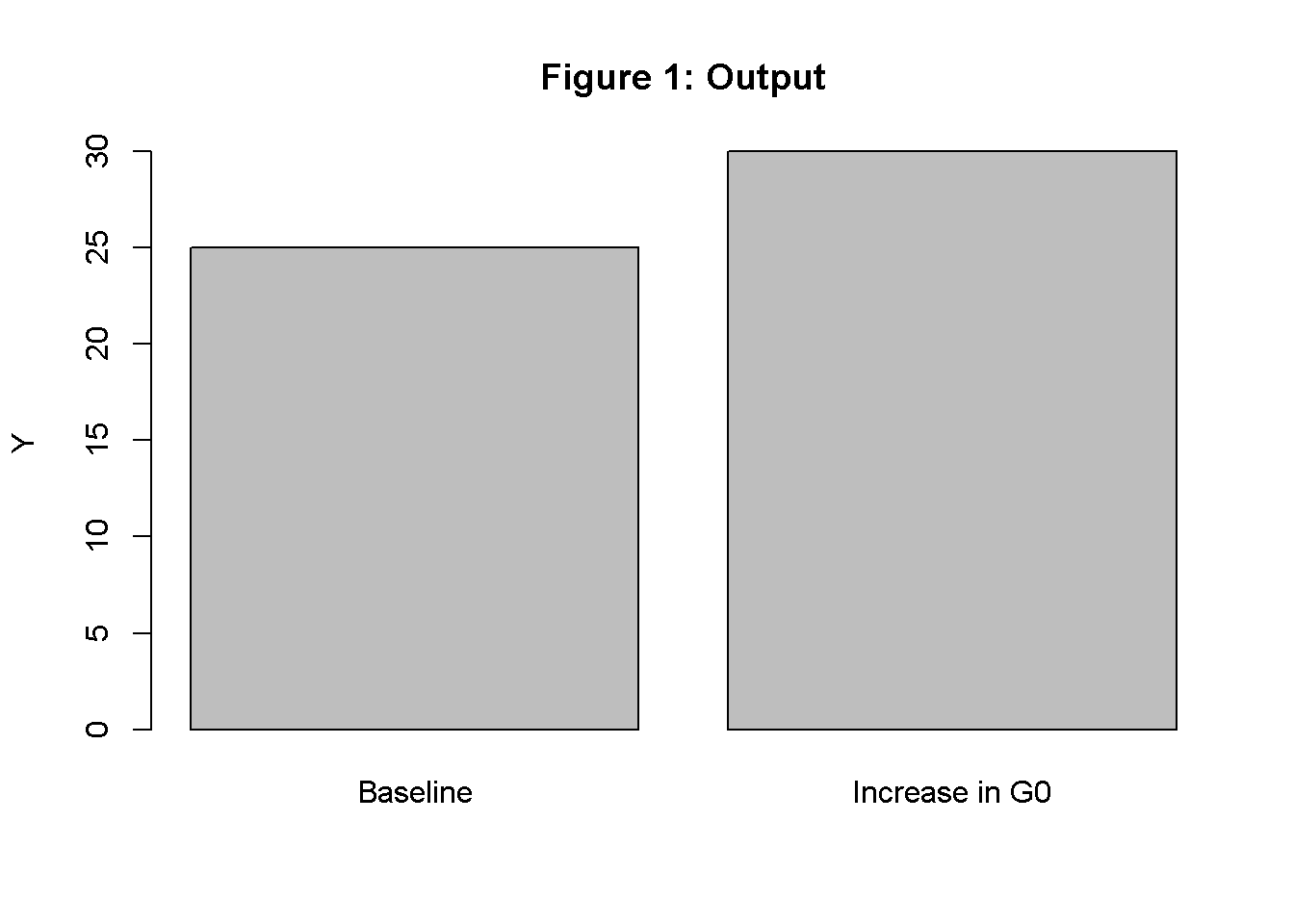

[1] 25 30

# Verify solutions for Y(G0[,Q])/(1-c1)

[1] 25 30

NotePython code

### Simulate Samuelson 1939# Set the number of periods for which you want to simulateQ =100# Set the number of parameterisations that will be consideredS =2# Set the period in which a shock or shift will occurs =15# Set fixed parameter valuesc1 =0.8beta =0.6# Construct (S x Q) matrices in which values for different periods will be stored; initialize at 1C = np.ones((S, Q))I = np.ones((S, Q))# Construct matrices for exogenous variables or parameters that will change # over time to capture different scenarios, initialise at 5G0 = np.ones((S, Q))*5# Set parameter values for different scenariosG0[1, s:Q] =6# scenario: permanent increase in government spending from G0=5 to G0=6 from period s=15 onwards# Solve this system recursively based on the initializationfor i inrange(S):for t inrange(1, Q): C[i, t] = c1 * (C[i, t -1] + I[i, t -1] + G0[i, t]) I[i, t] = beta * (c1 * (C[i, t -1] + I[i, t -1] + G0[i, t]) - C[i, t -1])# Calculate outputY = C + G0 + I# Display the solutions at time QY[:, Q -1]# Verify solutions for Y(G0[:,Q -1])/(1-c1)

The code solves the recursive system numerically through iteration. Let’s again break down what the code does:

set the number of periods for which we want to simulate the model (here \(Q=100\)), set the number of scenarios \(S\) and the period \(s\) in which a change in the scenario should occur

set the parameter values and create \((S \times Q)\) matrices in which the results for the endogenous variables will be stored, such that the columns represent time and the rows represent different scenarios; initialise the endogenous variables

define changes in exogenous variables or parameters (i.e. construct different scenarios)

write down the equations (solved for the endogenous variables such that every endogenous variable of the system appears on the left-hand side of an equation exactly once)

place these equations inside a for loop that runs from \(t=2\) to \(Q\)

the loop says: repeat the segment of code inside the curly brackets, each time with the index number \(t\) shifted by \(+1\) until \(t=Q\)

nest the loop that solves the system in an outer loop that loops through different parameterisations (here for \(G_0\))

Note that due to the exclusive presence of recursive equations, no loop is needed that iterates the equations within every period. However, many dynamic models contain both simultaneous and recursive equations. In this case, a third loop inside the time loop is needed that iterates the equations within each period so as to solve the simultaneous equations. Otherwise, the approach to solving dynamic systems is not fundamentally different from the one for static systems.

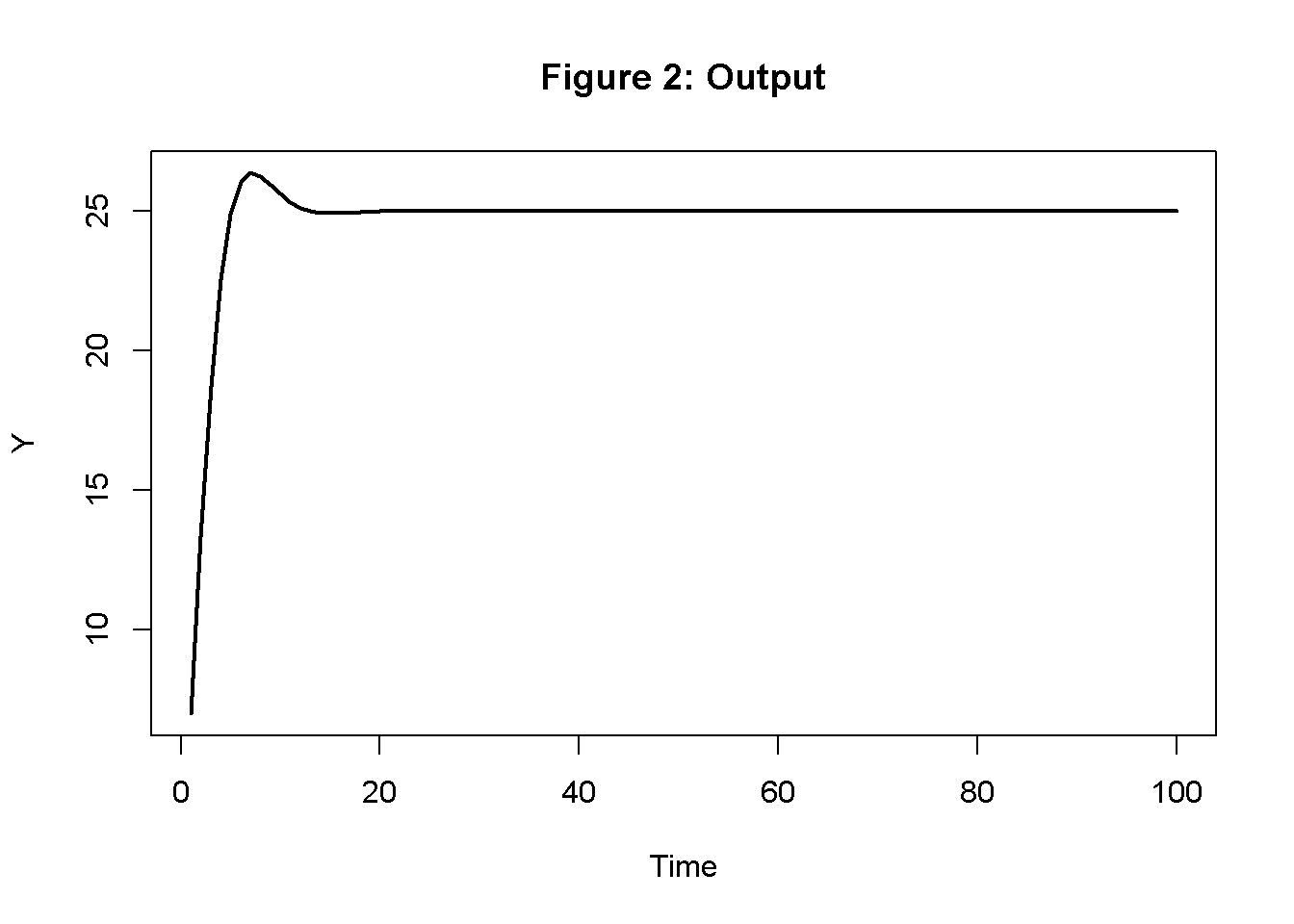

At the end of the simulation run, we can again compare the results from the numerical simulation with the analytical solution. However, what is perhaps more interesting is to trace the dynamic adjustment of the endogenous variables towards equilibrium. The best way to examine this is by plotting the results.

How to plot the results of a model

We will consider two main ways to plot model outputs: bar charts for static models and time series charts for dynamic models. Bar charts compare the equilibrium values of \(Y_t\) for different parameterisations:

# Bar chart of different equilibrium solutions of Samuelson (1939) modelbarplot(Y[,Q], ylab="Y", main="Output", names.arg=c("Baseline", "Increase in G0"))

Next, we show a basic version of a time series chart that displays the dynamics of \(Y_t\):

# Time series chart of output dynamics in Samuelson (1939) modelplot(Y[1, 1:100],type="l", col=1, lwd=2, lty=1, xlab="Time", ylab="Y")title(main="Output", cex=0.8)

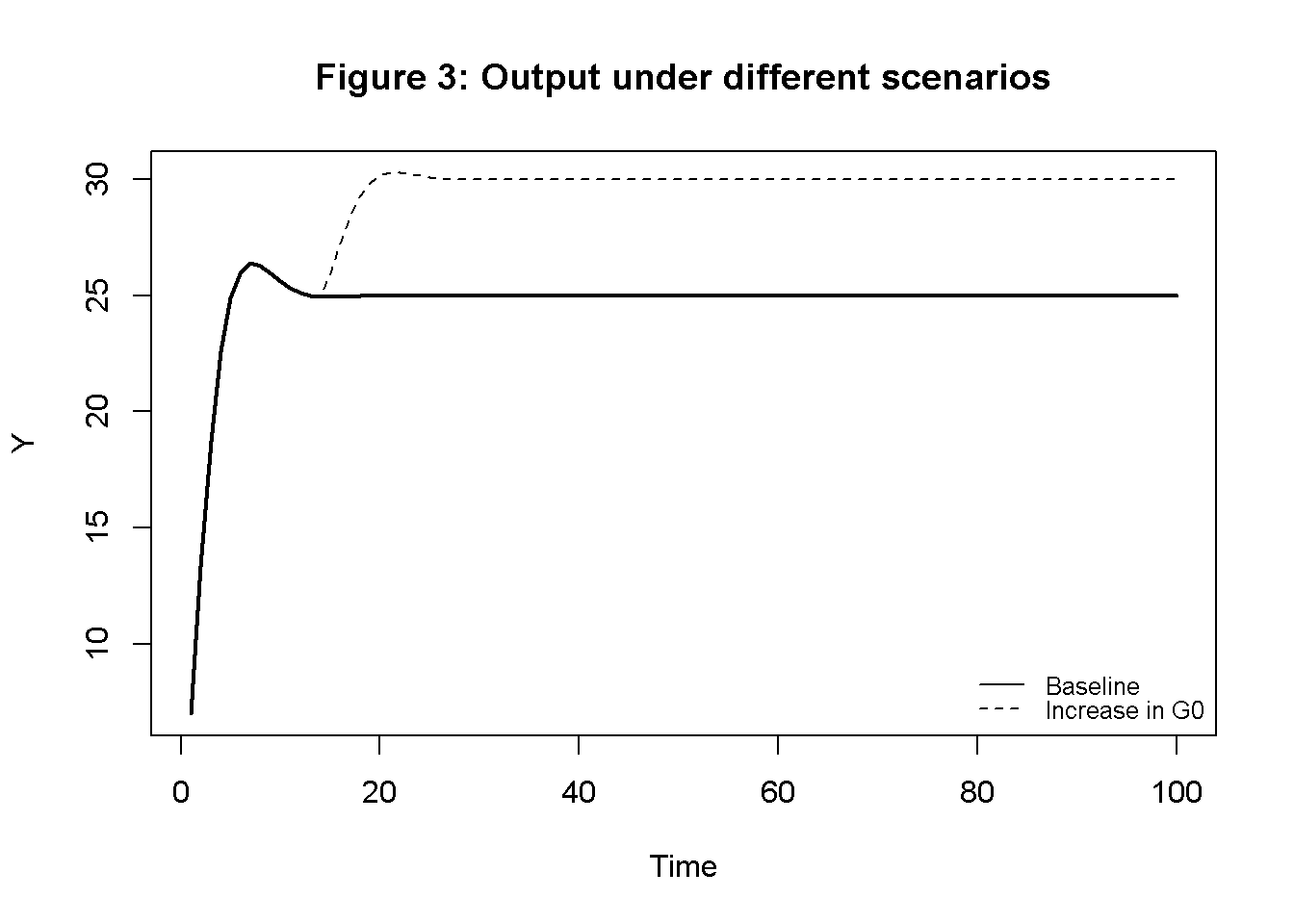

As you can see, there are many settings you can fiddle around with to adjust the appearance of the graph to your liking (run ‘?plot’ to find information about the different options.) If we want to plot the dynamics for the two different parameterisations, we can do the following:

# Time series chart of output dynamics for different scenarios in Samuelson (1939) modelplot(Y[1, 1:100],type="l", col=1, lwd=2, lty=1, xlab="Time", ylab="Y", ylim=range(min(Y[1,], Y[2,]), max(Y[1,], Y[2,])))title(main="Output under different scenarios", cex=0.8)lines(Y[2, 1:100],lty=2)legend("bottomright", legend=c("Baseline", "Increase in G0"), lty=1:2, cex=0.8, bty ="n", y.intersp=0.8)

Note that we have adjusted the range of the y-axis to make sure the graph captures the minimum and maximum values from both parameterisations.

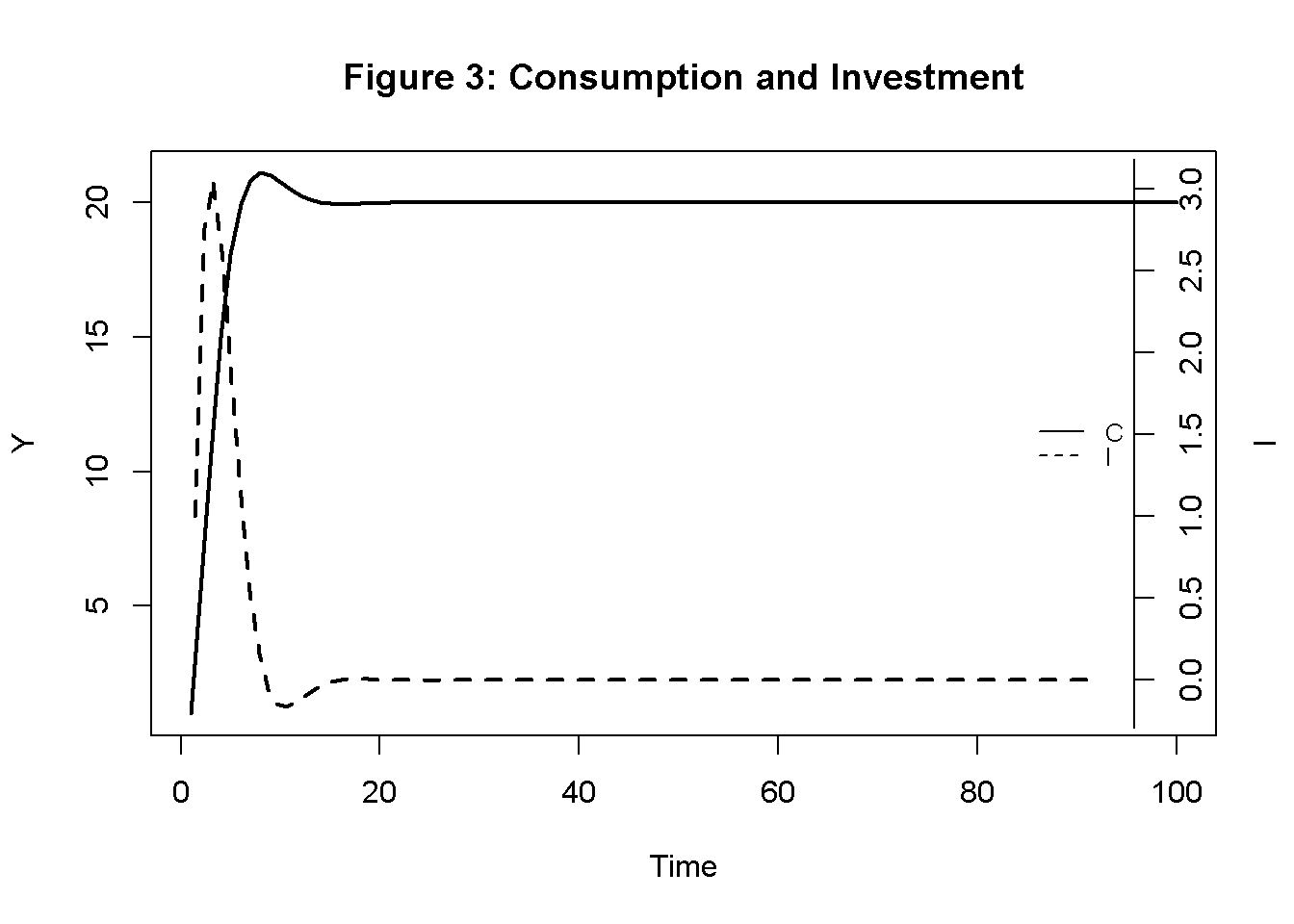

Finally, consider a plot for \(C_t\) and \(I_t\) with two separate axes:

# Time series chart of Samuelson (1939) model with separate axes for consumption and investmentplot(C[1, 1:100], type="l", col=1, lwd=2, lty=1, xlab="Time", ylab="Y")title(main="Consumption and Investment", cex=0.8)par(mar =c(5, 4, 4, 4)+0.3)par(new =TRUE)plot(I[1, 1:100], type="l", col=1, lwd=2, lty=2, font.main=1, cex.main=1,ylab ='', axes=FALSE, xlab ='', ylim =range(I[1, 1:100]), cex=0.8)axis(side =4, at=pretty(range(I[1, 1:100])), tcl =0.5)mtext("I", side =4, line =3)legend("right", legend=c("C", "I"), lty=1:2, cex=0.8, bty ="n", y.intersp=0.8)

NotePython code

#### Plots# Load matplot libraryimport matplotlib.pyplot as plt# Bar chart of different equilibrium solutions of Samuelson (1939) modelscenario_labels = ["Baseline", "Increase in G0"]plt.bar(scenario_labels, Y[:, Q -1])plt.xlabel("Scenario")plt.ylabel("Y")plt.title("Output")plt.show()# Time series chart of output dynamics in Samuelson (1939) modelplt.plot(range(1, Q), Y[0, 0:Q -1], color='black', linewidth=2, linestyle='-')plt.xlabel("Time")plt.ylabel("Y")plt.title("Output", fontsize=10)plt.show()# Time series chart of output dynamics for different scenarios in Samuelson #(1939) modelplt.plot(range(1, Q), Y[0, 0:Q -1], color='black', linewidth=1, linestyle='-')plt.plot(range(1, Q), Y[1, 0:Q -1], color='black', linewidth=1, linestyle='--')plt.xlabel("Time")plt.ylabel("Y")plt.title("Output under different scenarios", fontsize=10)plt.legend(["Baseline", "Increase in G0"], loc='lower right')plt.show()# Time series chart of Samuelson (1939) model with separate axes for consumption # and investmentfig, ax1 = plt.subplots()ax1.plot(range(1, Q), C[0, 0:Q -1], color='black', linewidth=2, linestyle='-', label='C')ax1.set_xlabel("Time")ax1.set_ylabel("C", color='black')ax1.tick_params(axis='y', labelcolor='black')ax2 = ax1.twinx()ax2.plot(range(1, Q), I[0, 0:Q -1], color='black', linewidth=2, linestyle='--', label='I')ax2.set_ylabel("I", color='black')ax2.tick_params(axis='y', labelcolor='black')plt.title("Consumption and Investment", fontsize=10)lines, labels = ax1.get_legend_handles_labels()lines2, labels2 = ax2.get_legend_handles_labels()ax2.legend(lines + lines2, labels + labels2, loc='right')plt.show()

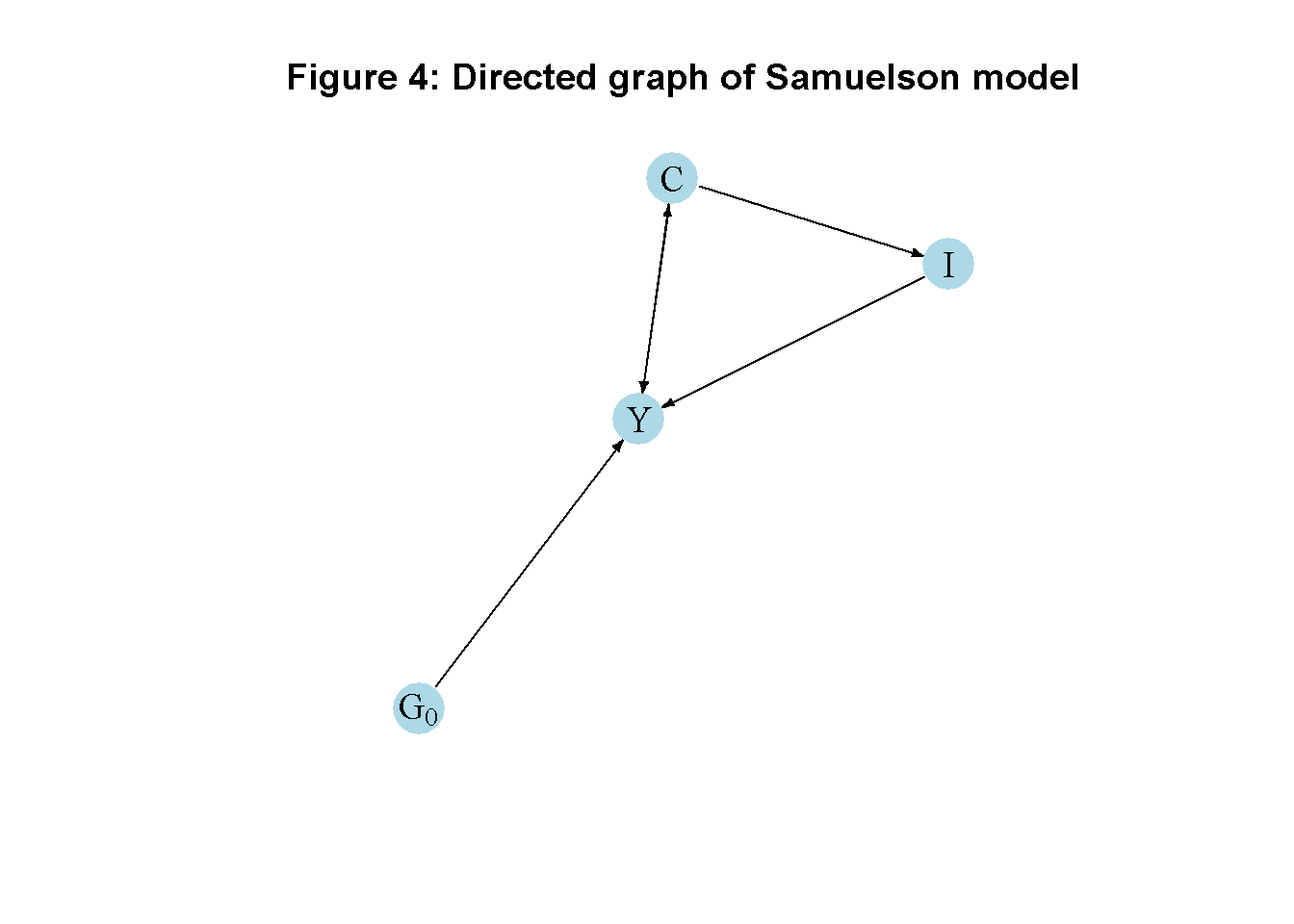

How to create a directed graph of a model

Another perspective on a model’s properties is provided by its directed graph. A directed graph consists of a set of nodes that represent the variables of the model. Nodes are connected by directed edges. An edge directed from a node \(x_1\) to node \(x_2\) indicates a causal impact of \(x_1\) on \(x_2\).

The directed graph can be derived from the model’s Jacobian matrix.2 Let \(x\) be the vector containing the model’s endogenous variables and \(f(x)\) the system of equations making up the model. The Jacobian matrix is then given by \(J=\frac{\partial f(x)}{\partial x}\). As we often also want to display exogenous variables in the directed graph, it can be useful to expand the Jacobian matrix by adding rows and columns for those exogenous variables.

Next, construct an ‘auxiliary’ Jacobian matrix \(M\) in which all the non-zero elements of the Jacobian are replaced by ones, whereas zero elements remain unchanged, i.e.

Finally, taking the transpose of this ‘auxiliary’ Jacobian matrix yields the adjacency matrix\(A=M^T\), which is a binary matrix whose elements (\(A_{ji}\)) indicate whether there is a directed edge from a node \(x_j\) to node \(x_i\). From the adjacency matrix, the directed graph is constructed.

The code below shows this for the example of the Samuelson (1939) model.3

## Create directed graph# Construct auxiliary Jacobian matrix for 4 variables: # endogenous: (1) Y, (2) C, (3) I# exogenous: (4) G0# where non-zero elements in regular Jacobian are set to 1 and zero elements are unchanged# Y C I G0M_mat=matrix(c(0, 1, 1, 1, # Y1, 0, 0, 0, # C0, 1, 0, 0, # I0, 0, 0, 0),# G0 4, 4, byrow=TRUE)# Create adjacency matrix from transpose of auxiliary Jacobian and add column namesA_mat=t(M_mat)# Create directed graph from adjacency matrixlibrary(igraph)dg=graph_from_adjacency_matrix(A_mat, mode="directed", weighted=NULL)# Define node labelsV(dg)$name=c("Y", "C", "I", expression(G[0]))# Plot directed graph matrixplot(dg, main="Directed graph of Samuelson model", vertex.size=20, vertex.color="lightblue", vertex.label.color="black", edge.arrow.size=0.3, edge.width=1.1, edge.size=1.2, edge.arrow.width=1.2, edge.color="black", vertex.label.cex=1.2, vertex.frame.color="NA", margin=-0.08)

NotePython code

#Load relevant librariesimport networkx as nximport matplotlib.pyplot as pltimport numpy as np# Construct auxiliary Jacobian matrix for 4 variables# endogenous: (1) Y, (2) C, (3) I# exogenous: (4) G0# where non-zero elements in regular Jacobian are set to 1 and zero elements are# unchangedM_mat = np.array([[0, 1, 1, 1], [1, 0, 0, 0], [0, 1, 0, 0], [0, 0, 0, 0]])# Create adjacency matrix from transpose of auxiliary Jacobian and add column namesA_mat = M_mat.transpose()# Create the graph from the adjacency matrixG = nx.DiGraph(A_mat)# Define node labelsnodelabs = {0: "Y", 1: "C", 2: "I", 3: "$G_0$"}# Plot the directed graphpos = nx.spring_layout(G, seed=42) nx.draw(G, pos, with_labels=True, labels=nodelabs, node_size=500, node_color='lightblue', font_size=10)edge_labels = {(u, v): ''for u, v in G.edges}nx.draw_networkx_edge_labels(G, pos, edge_labels=edge_labels, font_color='black')plt.title("Directed graph of Samuelson model", fontsize=12)plt.axis('off')plt.show()

Broadly speaking, three types of nodes are possible:

nodes from which arrows only point away represent exogenous variables (\(G_0\))

nodes towards which some arrows point, but from which arrows also point away, represent endogenous variables that also have a causal impact on other variables (\(Y\), \(C\), and \(I\))

nodes arrows only point towards represent endogenous variables that are residuals

It can thus be seen that the key exogenous variable in the Samuelson (1939) model is government spending \(G_0\), which determines aggregate income, which in turn feeds into consumption. Consumption then feeds into investment, which feeds back into income yielding the multiplier-accelerator effect.

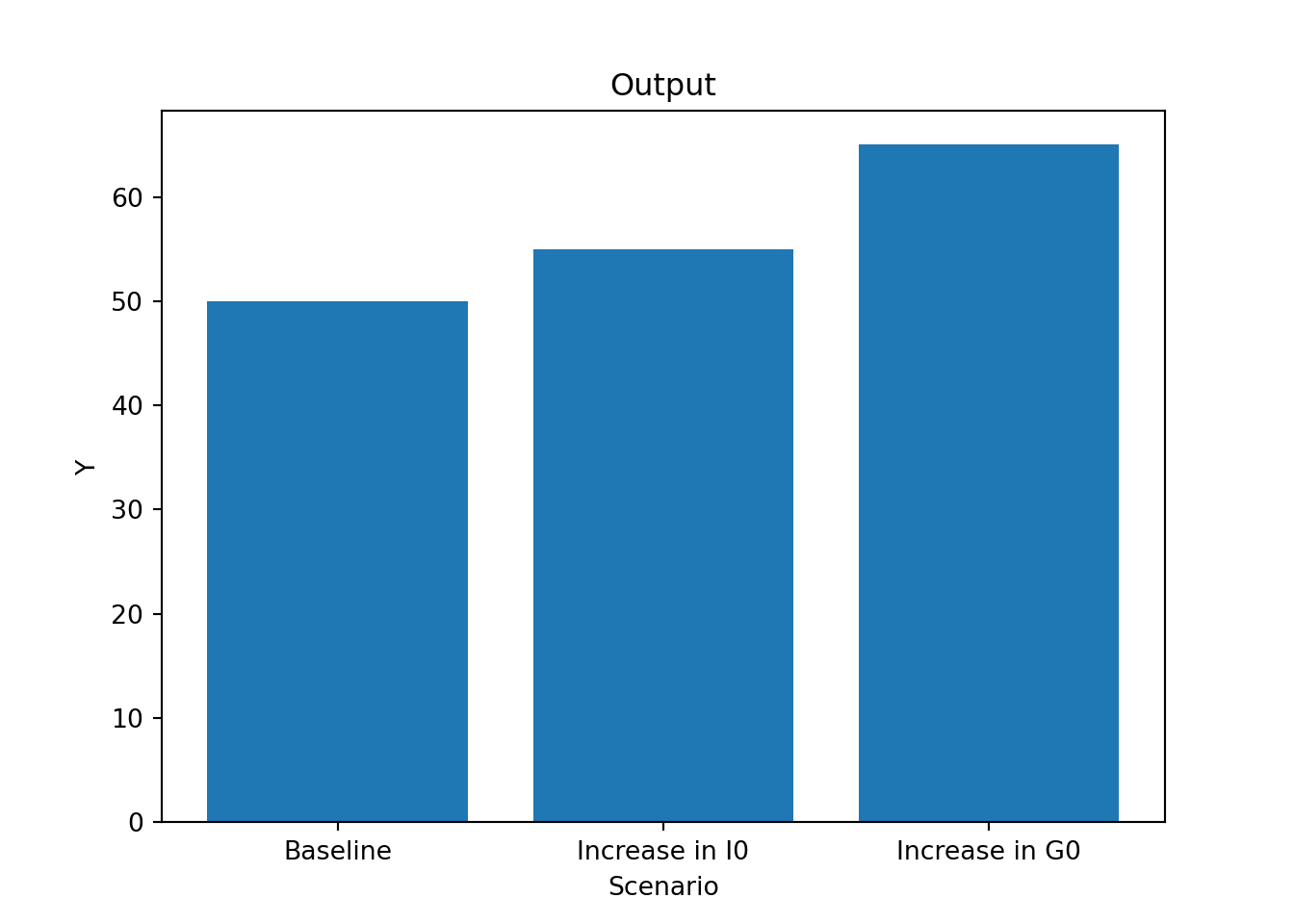

Exercise: simulating and visualising a simple model

take the code for the static Keynesian goods market from Section 2.2.1.1 above

add exogenous investment \(I_0\) to aggregate demand

set \(I_0 = 2\)

create a third scenario where \(I_0\) increases to \(I_0=5\)

plot equilibrium output \(Y^*\) for the three scenarios in a bar chart

TipR solution

### Add government spending to Keynesian goods market model#Clear the environment rm(list=ls(all=TRUE))# Set number of parameterisations that will be consideredS=3# Set fixed parameter valuesc0=3c1=0.8#Create vector in which equilibrium solutions from different parameterisations will be storedY_eq=vector(length=S)C_eq=vector(length=S)#Create vectors with parameters that will change G0=vector(length=S)G0[]=5# set G0=5 across all scenariosG0[2]=6# adding investment spendingI0=vector(length=S)I0[]=2# set I0=2 across all scenariosI0[3]=5# set I0=5 in third scenario# Initialise endogenous variables at arbitrary positive value Y=C=1#Solve this system numerically through 1000 iterations based on the initialisationfor(iin1:S){for(iterationin1:1000){Y=C+G0[i]+I0[i]# add investment to aggregate demandC=c0+c1*Y}# close iterations loop#Save results for different parameterisations in vectorY_eq[i]=YC_eq[i]=C}# close parameterisations loop# Bar chart of different scenarios for outputbarplot(Y_eq, ylab="Y", main="Output", names.arg=c("Baseline", "Increase in G0", "Increase in I0"))

TipPython Solution

### Add government spending to Keynesian goods market model# Set the number of parameterisations that will be consideredS =3# Set fixed parameter valuesc0 =3c1 =0.8# Create numpy arrays in which equilibrium solutions from different parameterisations will be storedY_eq = np.zeros(S)C_eq = np.zeros(S)# Create a numpy array with the parameter that will changeG0 = np.zeros(S)G0[:] =5# set G0=5 across all scenariosG0[1] =6# adding investmentI0 = np.zeros(S)I0[:] =2# set I0=2 across all scenariosI0[2] =5# set I0=5 in third scenario# Initialize endogenous variables at an arbitrary positive valueY = C =1# Solve this system numerically through 1000 iterations based on the initializationfor i inrange(S):for iteration inrange(1000): Y = C + G0[i] + I0[i] # add investment to aggregate demand C = c0 + c1 * Y# Save results for different parameterisations in the numpy arrays Y_eq[i] = Y C_eq[i] = C# Load matplot libraryimport matplotlib.pyplot as plt# Bar chart of different scenarios for outputscenario_labels = ["Baseline", "Increase in G0", "Increase in I0"]plt.bar(scenario_labels, Y_eq)plt.xlabel("Scenario")plt.ylabel("Y")plt.title("Output")plt.show()

Appendix: How to simulate dynamic model in continuous time

Sometimes, dynamic economic models are written in continuous time where the time increment is assumed to be infinitesimally small. Consider, for example, a continuous-time version of a Keynesian goods market model:

\[

\dot{Y}= k(C + G_0 - Y)

\]

\[

C = c_0 + c_1Y,

\] where \(\dot{Y}=\frac{dY}{dt}\). To simulate this model, we have to approximate the differential equation for \(\dot{Y}\) by a difference equation for \(Y_t\) and let the time increment \(\Delta t\) become very small. More specifically, we write:

\[

Y(t+\Delta t)=Y_t + \dot{Y} \Delta t =Y_t + [k(C + G_0 - Y)]\Delta t.

\] This approach is also called the Euler forward method. The code below shows to implement that method. We use \(\Delta t = 0.01\). Note that we need to raise the time horizon \(Q\) and set the adjustment speed \(k\) relatively high to make sure that the system has effectively converged to the equilibrium by \(Q\).

### Simulate continuous time version of Keynesian goods market model#Clear the environment rm(list=ls(all=TRUE))# Set number of periods for which you want to simulateQ=800# Set number of parameterisations that will be consideredS=1# Set fixed parameter valuesc0=3c1=0.8k=8delta=0.01# Construct matrices in which values for different periods will be stored; initialise at 1Y=matrix(data=1, nrow=S, ncol=Q)C=matrix(data=1, nrow=S, ncol=Q)#Construct matrices for exogenous variable G0=matrix(data=5, nrow=S, ncol=Q)#Solve this system recursively based on the initialisationfor(tin2:Q){for(iterationsin1:1000){Y[1,t]=Y[1,t-1]+delta*(k*(C[1,t-1]+G0[1,t-1]-Y[1,t-1]))C[1,t]=c0+c1*Y[1,t]}# close within-period loop}# close time loop# Verify solutions for Y(c0+G0[1,Q])/(1-c1)

[1] 40

Y[1,Q]

[1] 39.9999

NotePython code

### Simulate continuous time version of Keynesian goods market model# Load NumPyimport numpy as np# Set number of periods for which you want to simulateQ =800# Set number of parameterizations that will be consideredS =1# Set fixed parameter valuesc0 =3c1 =0.8k =8delta =0.01# Initialize matrices to store values for different periodsY = np.ones((S, Q))C = np.ones((S, Q))# Initialize the matrix for the exogenous variableG0 = np.full((S, Q), 5)# Solve this system recursively based on the initializationfor t inrange(1, Q):for iterations inrange(1000): Y[0, t] = Y[0, t -1] + delta * (k * (C[0, t -1] + G0[0, t -1] - Y[0, t -1])) C[0, t] = c0 + c1 * Y[0, t]# Verify the solution for Y at time Q(c0 + G0[0, Q -1]) / (1- c1)Y[0,Q -1]

References

Chiang, Alpha C, and Kevin Wainwright. 2005. Fundamental Methods of Mathematical Economics. 4th ed. McGraw-Hill Education.

Fennell, Peter G., David J. P. O’Sullivan, Antoine Godin, and Stephen Kinsella. 2015. “Is It Possible to Visualise Any Stock Flow Consistent Model as a Directed Acyclic Graph?”Computational Economics 48 (2): 307–16. https://doi.org/10.1007/s10614-015-9521-8.

Samuelson, Paul A. 1939. “Interactions between the Multiplier Analysis and the Principle of Acceleration.”The Review of Economics and Statistics 21 (2): 75–78. https://doi.org/10.2307/1927758.

That raises the question of whether an equilibrium is stable or unstable, which is discussed in Chapter 9.↩︎

See Fennell et al. (2015) for a neat exposition.↩︎

To create the directed graph, we rely on external libraries which you may have to install first. In R, this can be accomplished with install.packages("igraph") and in Python with pip install networkx. Once that library is installed, you only need to activate it in each session before you use it. In R, you can do this by executing library(igraph) and in Python through import networkx.↩︎